How to know what to spend when.

Retirement is a significant life transition that often evokes a mix of excitement and apprehension. As individuals approach this milestone, they are faced with a myriad of questions and concerns, ranging from timing their exit from the workforce to envisioning their post-retirement lifestyle. A common question we receive centers around withdrawals, and how to ensure the funds last through retirement. Keep reading! We have you covered.

In the pursuit of a secure and fulfilling retirement, effective management of assets plays a pivotal role. Understanding how to leverage these assets to sustainably support one's lifestyle while preserving financial security is paramount. In our exploration of retirement planning, we delve into the concept of withdrawal rates—a key metric that shapes the longevity of retirement savings.

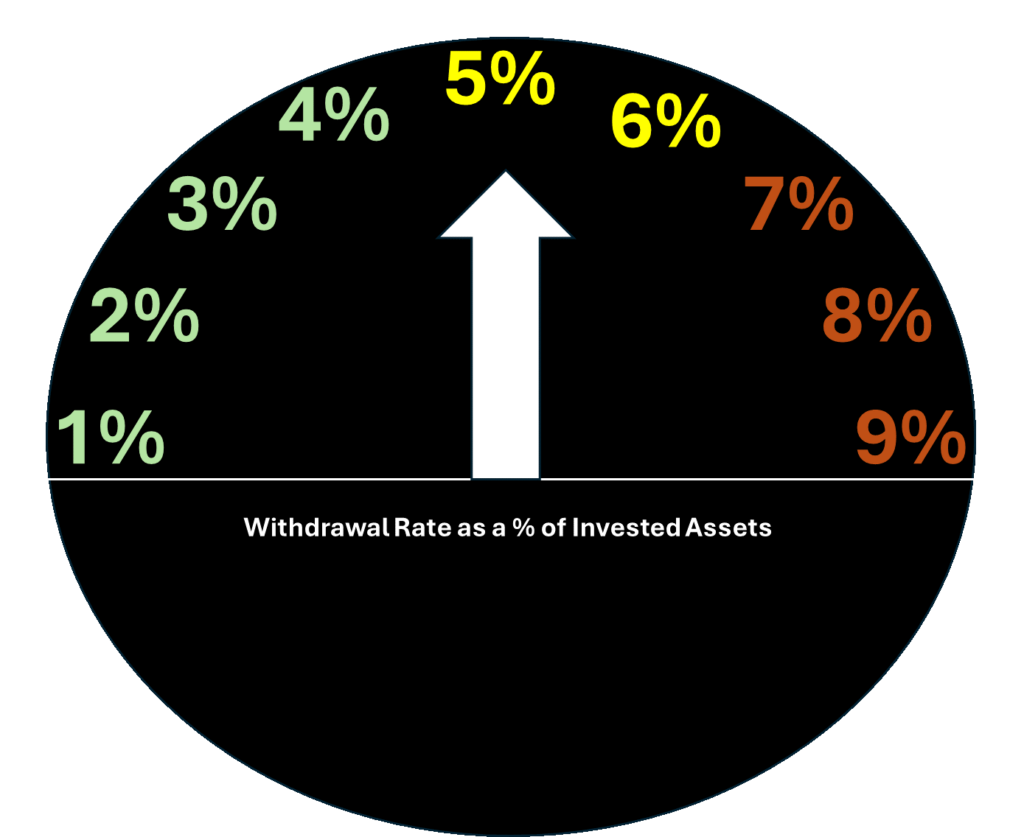

Imagine your retirement savings as a car journey, with the withdrawal rate serving as the speedometer. At lower withdrawal rates, akin to cruising at a moderate speed (1% to 4%), your assets are poised to endure the entire journey, with potential for growth along the way. This range aligns with conventional wisdom, offering a balance between meeting financial needs and safeguarding the longevity of retirement funds.

However, as the withdrawal rate climbs into the 5% to 6% range, it's like accelerating on the highway. While not immediately alarming, it warrants attention. At these speeds, the sustainability of your retirement savings may become less assured, with potential implications for long-term financial security. Vigilance and periodic reassessment are essential to navigate this terrain effectively.

Exceeding a 7% withdrawal rate is like pushing the pedal to the metal—a risky maneuver that could erode your retirement savings over time. Continuously drawing at such high rates may deplete your principal amount, compromising your financial resilience in the face of unforeseen expenses or economic downturns.

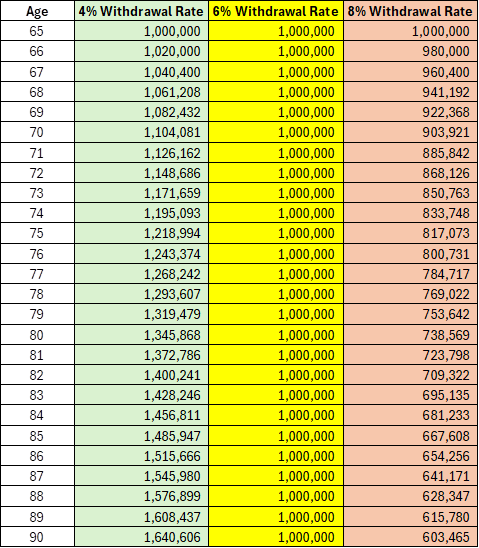

This chart breaks it down a little further:

Assuming a 6% rate of return in each scenario

It's important to note that retirement planning is a nuanced endeavor, shaped by individual circumstances and preferences. Factors such as risk tolerance, legacy goals, and lifestyle choices inform withdrawal strategies and asset management decisions. Moreover, staying attuned to market dynamics and adjusting withdrawal rates in response to changing conditions can enhance financial resilience and optimize retirement outcomes.

Ultimately, retirement planning is not merely about accumulating wealth but about deploying it strategically to sustain a fulfilling and financially secure lifestyle. By understanding the nuances of withdrawal rates and adopting a proactive approach to asset management, individuals can navigate the road to retirement with confidence and clarity.