When investing, it's common to think about diversifying within both your overall portfolio and each individual account. While this approach can work, we believe in going a step further and paying close attention to the details. Our CEO, Bobby Mascia, often says, "Diversification is lazy asset management." What he means is that you shouldn't diversify just for the sake of it. Instead, be strategic and invest in sectors or assets that are performing well. When market conditions change, you should adjust your investments accordingly. Additionally, consider whether your accounts are optimized to minimize tax impact. Let's dive deeper into what this means.

Asset Types

Account Types

Asset Location Tax Optimization Examples

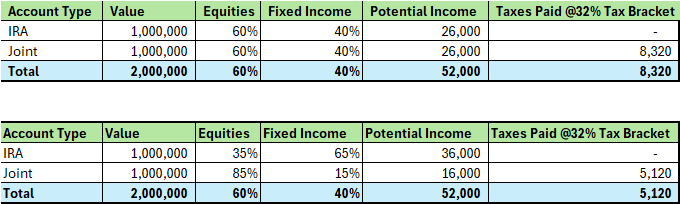

Let's use simple examples to illustrate the point. Both portfolios below have a value of $2 million, with a standard 60/40 allocation (60% equities, 40% fixed income).

Example 1: In this portfolio, the IRA and the Joint account are allocated the same amount to equities and fixed income (60/40). The joint account produces $26k of annual income, which is taxed at your ordinary income tax rate.

Example 2: The joint account has a higher percentage of equities, and the IRA has a higher percentage of fixed income. The overall allocation remains the same (60/40). Here, the joint account produces only $16,000 of annual income.

By thoughtfully considering the taxability of the assets in your portfolio, you can lower your tax burden not just in a single year but over time. In this example, you reduce your taxable income by $10,000 through optimizing the types of accounts and the taxability of the assets. This is done without changing the overall risk or return potential of the entire portfolio.

Key Assumptions

This can get more complex, especially as you dig deeper to learn more about their appreciation or taxable income, but even a basic understanding can be very beneficial. If you have any questions or would like to discuss in more detail, feel free to reach out to us.

The foregoing mention of taxable income is in the appreciation of the portfolio and is not income withdrawn; taxation on that would be different. You are responsible for consulting your own tax advisor as to the tax consequences associated with any investment or option. The tax rules governing options are complex, change frequently and depend on the individual taxpayer's situation. These are all things to confirm with your tax advisor and should not be deemed as advice.