Why does it feel like we keep talking about the same stuff? Because the lead news and narrative remain unchanged. Why should we care? Well, because as news and variables change, we need to make sure we are digesting said news and turning it into advice for positioning portfolios. Main points to be considered:

“If landing on the moon wasn’t dramatic enough, why should not landing on it be?” – Apollo 13

What is a soft landing? Why have economists and market experts been talking about this “hard landing” or “soft landing” ad nauseum? What the heck is going on?!?

With the Federal Reserve fighting inflation with one of the most dramatic interest-rate cycles in history, the greatest concern was the havoc that higher rates would have on the economy. In fact, more than 70% of economists were predicting a recession in either late 2022 or early 2023. And yet, no recession has been announced. Here we are, three quarters of the way through 2023, the jobs market is still strong, inflation has come down (although remains high; more on that later), and the economy seems to be trudging along. For those obsessed with aeronautics, we might call this a soft landing. We certainly would not call it a crash landing, as many were predicting (cough, cough, Michael Burry).

Even though the environment has proven to be more resilient than most forecasted, the horizon is far from clear. Oil has surged back above 90 dollars a barrel, Congress threatens another government shutdown, the consumer is showing signs of fatigue, the jobs market shows strength, but hours worked tells a more troubling story, and many economists warn that the effects of higher interest rates has yet to have its full economic impact.

That’s a lot to worry about! But it’s not all bad news. Let’s look at the bright side, when interest rates are higher, investors’ fixed-income yields are also higher. Some Money Markets are currently yielding north of 5%, an incredible return for the lowest segment of risk. That makes for a reasonable parking spot when investing discomfort sets in.

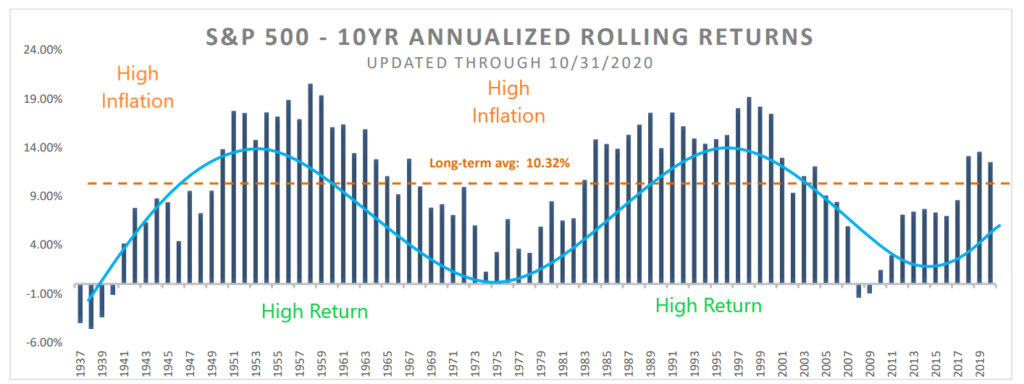

When you have a high rate of return on cash, it usually translates to a high rate of return on other assets. This is one of the positive impacts of shockingly-high inflation. It’s easy to focus on the immediate results of high inflation, but let’s not forget about the amazing returns that result after that high inflation dissipates.

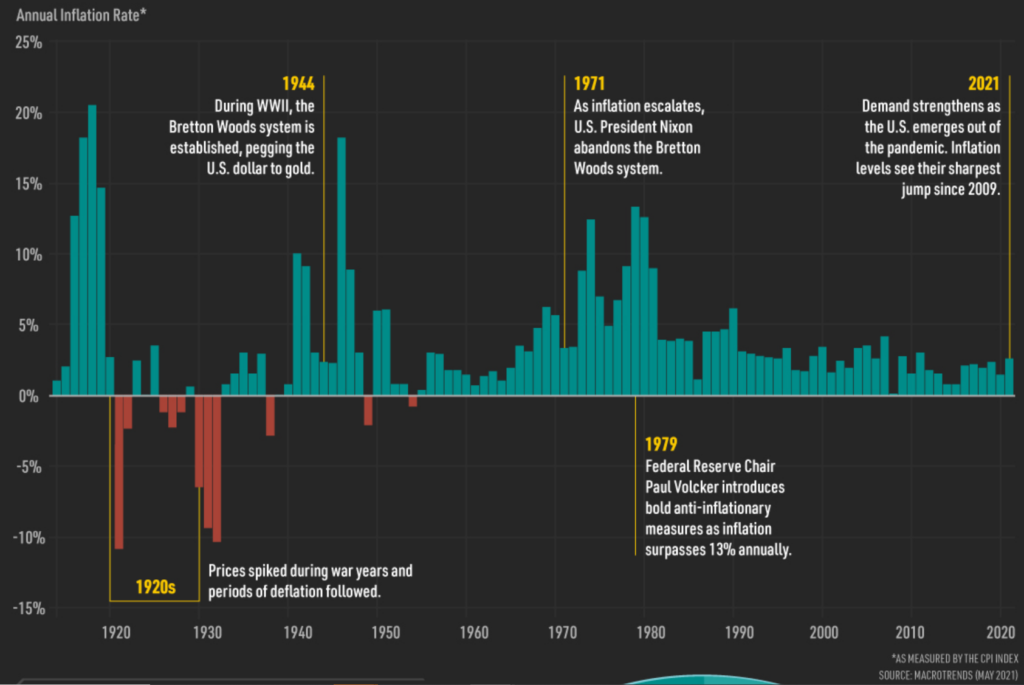

In the last 120 years, we have had three periods of high inflation. The first was during World War I, and the aftermath was the Roaring Twenties. The second was during World War II, and the aftermath was the Industrial Revolution during the 1950’s. The third was between 1970 to 1983, and while the cause of the inflation ranged, the 15 years after that inflation brought annualized market returns of over 14%. High inflation doesn’t necessarily cause high returns, but it causes innovation and productivity improvements that feed the next big wave of gains in the market.

So, while cash may offer an attractive return, don’t get too comfortable sitting there for too long. There may be great returns ahead once inflation tamps down and all the amazing innovation that we are seeing matures and delivers a positive impact!

Sources: Bloomberg (annual Inflation Rate) Macrotrends (S&P500 10yr Annualized Rolling Returns)

Sincerely,

Bobby, Jordan, and team