Navigating Social Security: A Guide to Maximizing Your Benefits

Social Security can make a big impact on your financial plan. Oftentimes, deciding when to start claiming the benefit can be overwhelming. Clients often ask us the following: Should I claim it as soon as I turn 62? Does it make sense to wait longer until full retirement age (see graph below)? What are the tax implications? Are there benefits to pushing it back to when I turn 70?

Our analysis below works to shed some light on the topic and includes tax implications, and the tools and information we use to answer those questions. Let’s start with the basics.

When can I start to take Social Security?

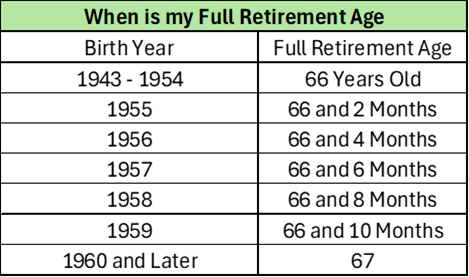

Age 62 is the earliest an individual is allowed to file for Social Security. While you can start taking Social Security at this age, you will have a reduced benefit compared to taking it later on and your monthly payments will be less than if you decided to wait until your Full Retirement Age or Age 70. Full Retirement Age is between 66 and 67 depending on the year you were born (see table). This is when you would receive your full benefit amount.

By delaying until age 70, you can further increase your benefit by a certain percentage each year. At age 70 you will have to file for Social Security, and this is the maximum amount of Social Security income you can receive.

What are the tax implications for Social Security income? The main tax implications to take note of are how much income you are making in a year while taking social security.

As you can see from the tables below the more income that you make, the higher percentage of your Social Security income will be taxed. The maximum amount of Social Security income that will be taxed is up to 85%.

This “85%” of your social security income will then be taxed at the ordinary income tax bracket that you fall under.

Analyzing when the best time to take Social Security: When we analyze the optimal time to take Social Security there are three main factors that we consider:

Immediate Income Needs

Longevity

The “Break-Even Point”

These three factors are crucial in deciding when to take Social Security and not something that can be determined without knowing more about an individual's specific circumstances. As such, financial planning is of the utmost importance to making these financial decisions take these nuances into consideration.

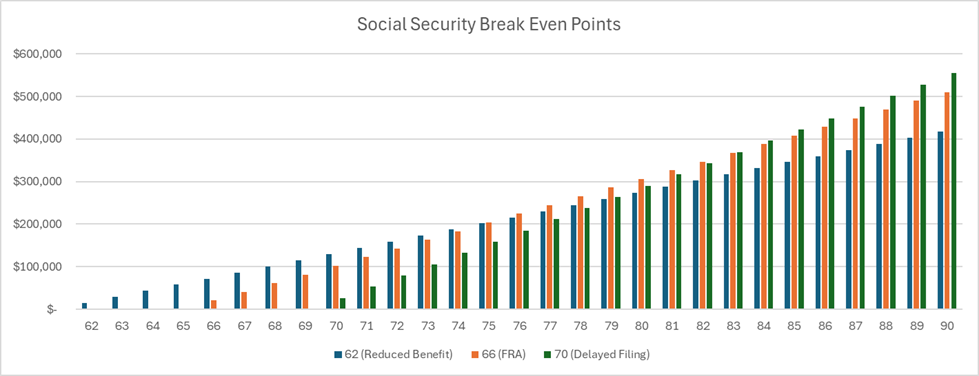

The chart below shows a simple example of how the break-even points work based on an individual's financial plan ending at 90 years old. The key takeaways are:

If you were to live until 90, waiting to file until 70 makes the most sense as you would accumulate over $100k more of income throughout the years compared to filing at 62 years old.

Comparing filing at 62 vs 70 the breakeven point is 83 years old which means at age 83 you would have accumulated more from waiting to file until age 70 than filing right away at 62 years old.

This table is a base-case scenario. Another factor we take into consideration is the spousal benefit, and how it applies to you and would affect the best age for you to file for social security.

Accumulated Income Overtime. Example $1,200 monthly income at 62, $1,700 monthly income at FRA, and $2,200 at age 70. Assuming 90 years old is the life of the plan.

It is always important to gain a better understanding of financial decisions. As always, we are here to light the way. Please let us know if you have any questions about Social Security or would like to schedule a meeting to discuss this in more detail.

Here are a few links to resources that are helpful to look over: