Punxsutawney Phil got it right in 2026; he saw his shadow and we got a month filled with turbulent weather, including arctic cold snaps and snowstorms. We also had some turbulent weather in the markets as we digested earnings, economic data, and a Supreme Court ruling that made another ripple in the tariff saga. Moreover, we continued to see investors buy up value, small-cap, and international stocks while selling the growth names that have been so popular in the last five years.

Performance (as of February 27, 2026; source ycharts.com)

| Month to Date | Year to Date | |

| S&P 500 | -0.8% | 0.7% |

| Nasdaq Composite | -3.3% | -2.4% |

| MSCI ACWI ex USA | 5.0% | 11.3% |

| Bloomberg US Aggregate Bond | 1.6% | 1.8% |

| Russell 1000 Value | 2.6% | 7.3% |

| Russell 1000 Growth | -3.4% | -4.8% |

| Russell 2000 (small cap) | 0.8% | 6.2% |

It is worth noting that the weakest markets above are the Russell 1000 Growth Index and the Nasdaq Composite (a growth-heavy index). One of the easiest ways to figure out why is to look at the year-to-date performance of the Magnificent 7 stocks:

| Alphabet | -0.4% |

| Meta | -1.8% |

| Apple | -2.8% |

| Nvidia | -5.0% |

| Amazon | -9.0% |

| Tesla | -10.5% |

| Microsoft | -18.8% |

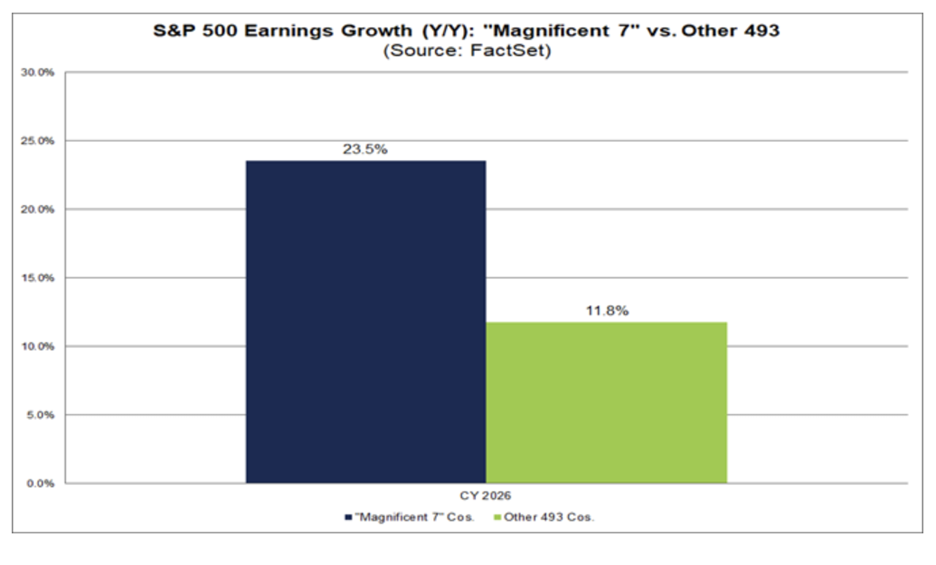

The weird thing about the Magnificent 7 being down year-to-date, while many other markets are up, is that their earnings were excellent. The actual reported earnings growth rate for the Magnificent 7 was 27.2% for the fourth quarter. The other 493 stocks in the S&P 500 had a blended earnings growth rate of 9.8% in the fourth quarter. It is amazing when seven companies are growing at almost three times the rate of the other stocks in the market and are down on the year. Obviously, one needs to consider where the stocks were valued when deciding how to react to earnings—but still!!!! Opportunity maybe?!?!

Overall, fourth quarter earnings have been strong. 96% of the companies have reported earnings as of the end of February, and so far, the blended year-over-year growth rate is 14.2% (the 5th consecutive quarter of double-digit earnings growth). To put this into context, the estimated growth rate at year end (December 31, 2025) was that the index would have an earnings growth rate of 8.3%.

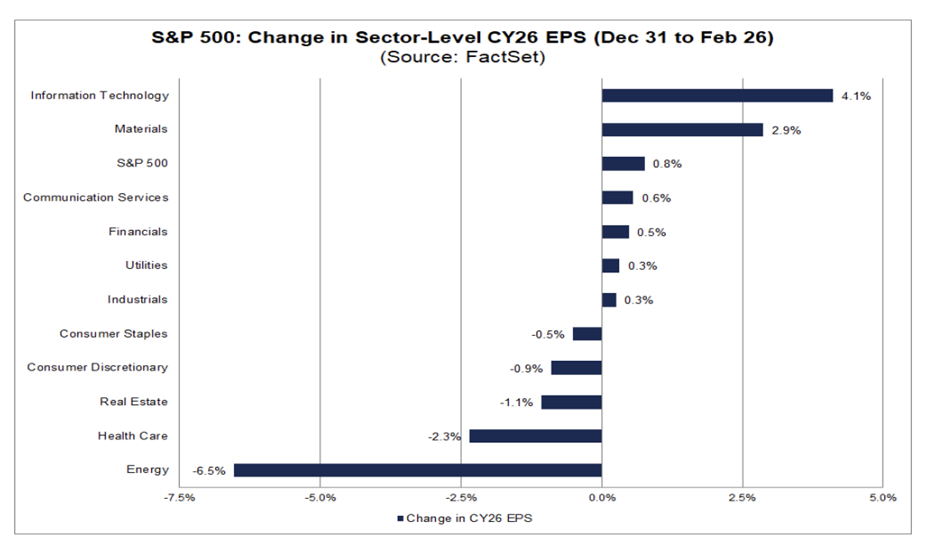

What is interesting is that the market seems more interested in stories than earnings at the moment. The beginning of the year had more scary stories about Artificial Intelligence, just like we had last year (recall DeepSeek) and more tariff drama. What is somewhat amazing is that if we look at the table below, which shows the change in earnings estimates for Calendar Year 2026, we see the following:

- While the Tech sector is DOWN 3.6% year to date, earnings estimates are UP 4.1% (the most positive revision of all the industry sectors).

- While the energy sector is UP 25.1% year to date, earnings estimates are DOWN 6.5% (the most negative revision of all the industry sectors).

Before I make everyone go cross-eyed from numbers and percentages, let me simplify the point I’m getting at:

- Magnificent 7 (and even most technology stocks) had great earnings but the market doesn’t seem to care. The market is back to being concerned about what the impact of Artificial Intelligence is going to be on the sector. Last time this happened (early 2025), it turned out to be a great buying opportunity.

- Earnings in general have been very strong, and the market tends to follow earnings in the long run. Don’t get caught up in the headlines and ignore the earnings!

The Economy: Economic numbers came in a bit mixed; GDP growth was revised upward for Q3 2025 to 4.4% and estimates for Q4 2025 are coming in at 2.2%. However, the jobs number was revised down to 181,000 for ALL of 2025, one of the lowest non-recessionary figures on record. Some are calling this “jobless growth”, which is another way to say productivity is soaring. You see, GDP growth comes from either 1) more workers or 2) more productivity. We can rule the workers out, so it must be a productivity boom. Is the Artificial Intelligence productivity boom already underway?!?!

Iran Strike: This is still a little too fresh to comment on, but the one predictable market reaction to conflict in the Middle East is OIL GOES UP. And we certainly saw oil go up. This may prove to be important because higher oil prices are inflationary, and the biggest reason to prevent the Federal Reserve from cutting rates in March would be inflation concerns. So, with the possibility of a drawn-out conflict and higher prices at the pump, this conflict is likely to make it harder for the Federal Reserve to move forward with a rate cut in the near future.

Tariffs (again!): The Supreme Court FINALLY ruled on Trump’s use of the International Emergency Economic Powers Act (IEEPA) to enact sweeping tariffs across the world. They ruled that Trump had exceeded his executive authority with these tariffs. And of course, Trump excepted the ruling and went about the rest of his day calmly……..HAHAHAHA!!!

What Trump actually did is immediately shift to using Section 122 of the Trade Act of 1974, which legally grants the President the right to enact tariffs for 150 days only. It limits the maximum tariff to 15%, although the administration announced a 10% tariff starting on February 24th.

Many questions remain about what is going to be done about the past tariffs that have now been confirmed by the Supreme Court to be illegal. It is likely to be messy, and it may turn into lengthy legal battles that last years. One thing is for certain, the Trump administration is not giving up on tariffs, and I would expect to see the administration continue to push for tariff policies. With the midterms coming up and the tariff policies being generally unpopular, it is hard to make any real predictions on how this story will play out.

Conclusion: It is worth repeating that year-to-date markets are mostly up, long-term interest rates are down, earnings have been great, and economic data is coming in suggesting continued growth. Of course, the attack on Iran at the end of the month introduced several new variables into the mix, and while we keep those in danger in our thoughts, investors should recognize that this will also likely create opportunities. We have said this in past commentaries, but it seems worth repeating at this stressful time; Spend as much time thinking about what can GO RIGHT as you do thinking about what can GO WRONG!

Jordan Kaufman

Chief Investment Officer

Green Ridge Wealth Planning

Disclosure:

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment/tax advice. The investment/tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment/tax strategy for his or her own particular situation before making any investment decision(s). You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning