With the exhilarating NY Knicks Championship run, the World Cup, and the 250th anniversary of the U.S., I have heard a lot of “you are watching history being made” types of comments. In markets, we are always looking for some historical context to understand events and market reactions. Below, we take a deeper dive given all the hype, concerns, and changes around Artificial Intelligence.

Market Performance through June 30, 2026:

- S&P 500: 10.2% year to date

- Nasdaq Composite: 13.1% year to date

- Bloomberg US Aggregate Bond: 0.6% year to date

- MSCI All World ex US: 14.0% year to date

- S&P GSCI Gold: -7.0% year to date

- PHLX Semiconductor Sector: 101.1% year to date

(source: ycharts.com)

Overall, equities are having a great year so far. But clearly it is not felt across all sectors or names. I added the Semiconductor index to highlight how some areas of the market are having a very different experience than the typical stock.

Using gold as an example, here we highlight some big changes. Gold was up over 23% for the year on January 2nd. It is currently negative on the year after suffering one of its worst monthly performances (down over 10%) since 2008. While the Federal Reserve’s hawkish stance on inflation, cooling oil prices, and de-escalating Middle East tensions are part of the cause for the move, it is a reminder how quickly things can shift in these markets.

Kevin Warsh and the New Mantra of the Federal Reserve

Things have changed rather quickly under new Federal Reserve Chair Kevin Warsh. The Federal Reserve statement, a document released after every Fed meeting, has been shortened to just 130 words from 300+. While one could call this just being more concise, the Federal Reserve is no longer giving forward guidance. The Federal Reserve also stated that inflation is too high and that they are committed to reducing inflation pressure. So, while they did away with guidance, they signaled that Wall Street and the economy should prepare for a possible rate hike; a big change from the possible rate cut everyone has been expecting this year.

I don’t want to dig too deep into this story, but watching Warsh engage in a question and answer session with the press was a very different experience from his predecessors. It felt much punchier and more assertive. His rationale for not giving forward guidance was a bit dizzying; he argued that Wall Street was just reacting to how the Fed would change its guidance, and that he wanted to see more authentic moves in the market. That is such a nice theory, but removing guidance adds to uncertainty, and if you add uncertainty to something, people tend to want to pay less for it. In this case, it would be U.S. assets. I don’t want to sound extreme, but I get worried when the Chair of the Federal Reserve seems head strong and starts arguing questionable logic. Let’s see where this goes.

Earnings Season Approaches!

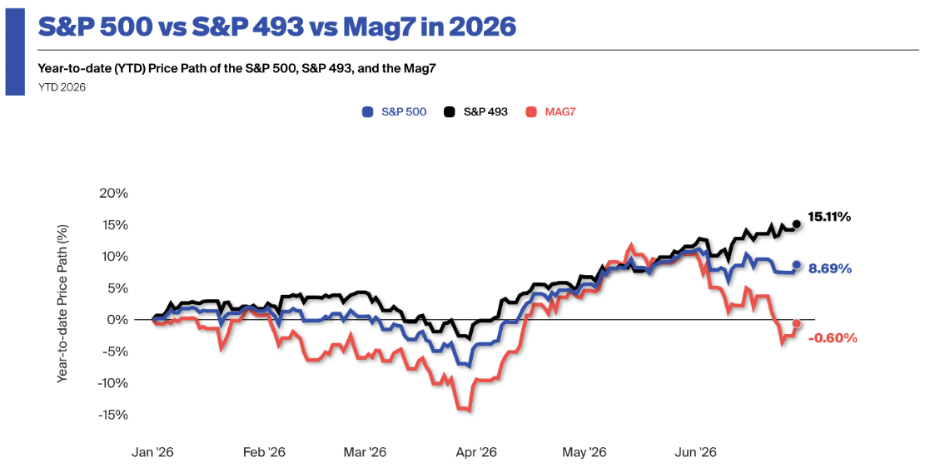

I am super excited for this earnings season! In recent quarters, the Magnificent 7 have led the way in earnings. The earnings growth rate in the first quarter of 2026 was 27.1% according to FactSet which was the highest recorded growth rate since the fourth quarter of 2021. But digging deeper, 71% of that net dollar-level increase was attributed to just three companies; Alphabet, Amazon, and Meta. The market seems unimpressed by these companies’ contributions, with Alphabet up around 11% as of June 30th for the year, Amazon up around 3%, and Meta down year to date. It is kind of crazy when these companies are performing so well on a fundamental basis. The chart below shows how the Magnificent 7 stocks (Tesla, Amazon, Alphabet, Apple, Microsoft, Meta, Nvidia) have lagged behind the other 493 stocks in the S&P 500.

Source: https://chartkidmatt.com/p/10-reasons-to-be-bullish

So, if the Magnificent 7 have such strong earnings, why are their stocks not reflecting it? The answer is that there is significant concern that they are over investing in Capital Expenditures (CapEx) for future compute in Artificial Intelligence with no real plan to pay back the investment. This concern is reminiscent of the 2000 Tech Bubble concern, and for those who are following closely, you will recognize that this is the conversation we need to have right now. Which brings us to our next topic…

Is the Artificial Intelligence Frenzy the Same as the Tech Bubble?

This is a hot topic, and of course we won’t know exactly until after the fact, but there are certainly distinct differences. We are seemingly approaching that point where investors are starting to demand to see valuations supported by actual productivity gains, not just momentum and headlines.

- Valuation Parallels but Different Fundamentals: The AI leaders exhibit some similarities to the leaders during the Tech Bubble (high growth expectations, new technology narratives, retail enthusiasm), but today’s public stocks that are AI leaders have high revenue and profits. During the Tech Bubble, many of the leaders did not make money or profits. Some of the private AI companies are still struggling to make profits, and investors need to continue to watch closely to see how that evolves over time. For example, OpenAI had revenue of $13 billion in 2025, but in January the company itself projected an operating loss of over $14 billion in 2026, and some analysts predict it could be much higher. Source

- The Productivity Question: During the Tech Bubble, productivity gains did not materialize at the level and timeframe investors expected. There is concern this could be true with AI companies as well, however signs point to some improvement in the projections for productivity and capital returns. The question remains: are current valuations pricing in realistic productivity improvements or is there still too much fantasy priced in?

I don’t want to get in the prediction game, but it is worth discussing the difference between a bad vs. good CapEx investment. The 10-year bond yield is currently 4.5%. Any company investment must have a better ROI than 4.5% to be considered productive, assuming the same amount of risk. Of course, data centers and compute investments are riskier than a treasury bond investment, so they must yield higher returns than a 10-year treasury bond to be worthy of the associated risk.

So, What are People Saying About the CAPEX of These AI Hyperscalers?

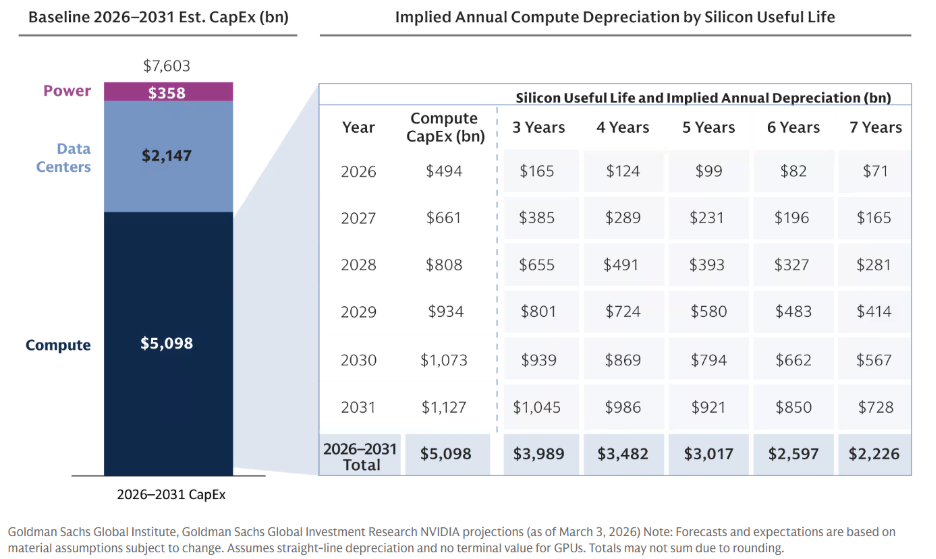

The Magnificent 7 are spending at unprecedented rates to build out AI data centers and computing capacity. This capital allocation decision is perhaps the most important investment thesis of 2026! It is also one of the most uncertain. Current estimates for CapEx for AI infrastructure now exceed $700 Billion for the hyperscalers. Goldman Sachs released an article estimating an aggregate infrastructure spend of $7.6 trillion through 2031. That is a lot of money, and they break it down in the table below.

Compute is the largest contributor to the total CapEx, and that helps explain why the semiconductor sector is up so much year to date. When looking through some analyst reports on the CapEx spending versus payback periods, estimates range between a bullish two-year payback to a more bearish seven-year payback (or worse!). That is really where the rubber is going to meet the road: How long are we going to have to wait to see the return on this huge investment? I expect investors to get impatient, and that is likely to make this a bumpy ride with so much of current valuations being based on future performance.

Conclusion

There is still a lot to watch, but we think the dominant story to keep your eye on is whether or not we start to see real profits created from AI investments. That is what makes every earning season important to watch carefully as investors are going to be reading the tea leaves. In particular, keep an eye on management comments around CapEx and Cloud division growth numbers.

The outcome of the AI story will be what decides the next 5 to 10 years of returns for equities, so it is important to stay fixated on what is happening there. Try not to get too distracted by the cyclical stories like the Iran conflict or NATO summits. There is a real secular story happening, and it could change everything. If you need help thinking it all through, give us a call. WE LOVE THIS STUFF!

Have a great summer!

Chief Investment Officer

Green Ridge Wealth Planning

Disclosure:

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment/tax advice. The investment/tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment/tax strategy for his or her own particular situation before making any investment decision(s). You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning