We just went through a volatile 2025, and with how 2026 is starting, now is not the time to loosen your seatbelt or get up and walk around the cabin. January alone delivered a handful of unpredictable headlines that have understandably left some investors confused. So, let’s not waste any time jumping in—because in a week, this news will be stale, and we’ll likely be reacting to something entirely different. These days, our news cycle seems to have the same shelf life as an avocado.

Year-to-Date Performance

- S&P 500: 1.5%

- Nasdaq Composite: 1.0%

- MSCI ACWI ex-U.S.: 6.0%

- Bloomberg U.S. Aggregate Bond: 0.1%

- Source: YCharts (as of January 31, 2026)

A few takeaways from the numbers above:

- We’re up across the board in most markets. Given some of the more dramatic headlines to start the year, that’s impressive. This shouldn’t come as a huge shock if you’ve been paying attention to earnings.

- International equities are the early standouts. This outperformance was helped by a weaker dollar, along with several structural and fundamental factors that could continue to support international stocks after a strong showing in 2025.

The Economy

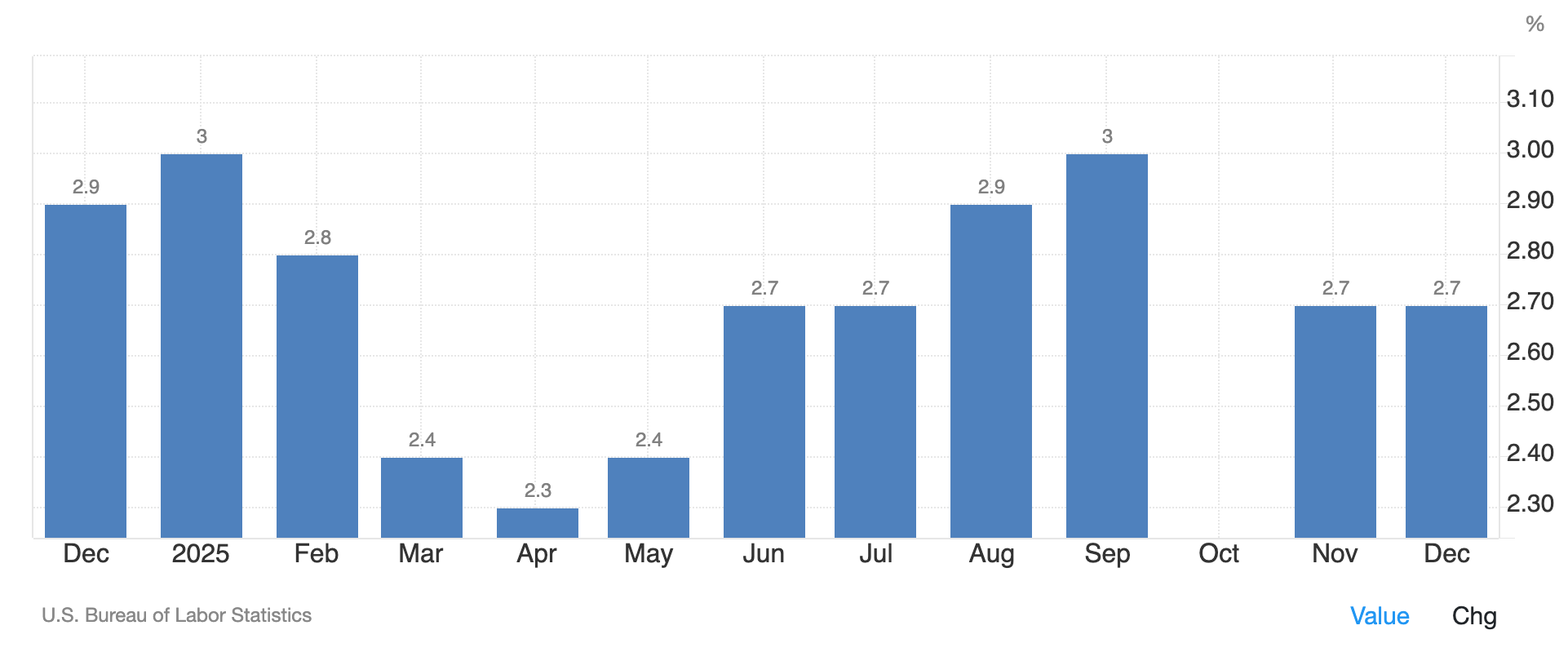

Overall, economic data remains fairly stable. The unemployment rate is hovering around 4.4%, and inflation continues to be sticky, holding close to 3% on the Consumer Price Index. While inflation isn’t back to anyone’s “ideal” level, things aren’t terrible. So far, changes in inflation have been relatively modest outside of the March–May dip tied to Liberation Day volatility.

Source: Trading Economics

That said, government shutdowns and rapidly shifting fiscal politics make it difficult to put too much weight on any single economic data point. From an investment perspective, stability—boring as it may sound—is generally a positive signal for markets.

Interest Rates

Interest rates moved slightly higher during January, but the bigger story came at the end of the month when Donald Trump announced his pick to lead the Federal Reserve starting in May 2026. This caught many by surprise, especially given Trump’s rhetoric over the past year.

Trump has been openly frustrated with current Fed Chair Jerome Powell for not cutting rates more aggressively, hoping that lower rates would help boost economic momentum during his term. Powell, and most of the Federal Open Market Committee, have remained cautious, citing concerns over tariffs and persistently sticky inflation. While markets once expected rate cuts early in 2025, the Fed ultimately delivered three cuts later in the year—in September, October, and December.

This announcement is particularly interesting given Trump’s pick: Kevin Warsh. Warsh has long been a critic of central banks distorting markets through zero interest rates and excess liquidity. He served on the Federal Reserve from 2006 to 2011 and was often outspoken in his criticism of post–financial crisis Fed policy. Given Trump’s recent comments about the Fed, Warsh was a very unexpected choice, as his history suggests he may not be especially quick to cut rates either.

From a “Fed independence” standpoint—a major concern toward the end of last year—this appointment is a meaningful positive for markets.

Earnings

Earnings continue to do the heavy lifting. About 33% of S&P 500 companies have reported so far, and results have been strong. According to FactSet, blended year-over-year earnings growth is tracking at 12%, roughly 4% higher than estimates at the end of December.

Even more impressive—the blended net profit margin is 13.2%—the highest margin FactSet has ever recorded for the index. There’s plenty of nuance to unpack in earnings season, but keeping it simple: fundamentals remain the engine pushing markets higher.

International Stocks

International stocks have lagged U.S. stocks for decades, but they outperformed the U.S. by more than 10% in 2025, and 2026 is shaping up to potentially tell a similar story. Several themes are driving this shift:

- Geopolitical uncertainty and concerns around U.S. trade policy

- A weaker U.S. dollar, which boosts foreign returns when translated back to dollars

- Investor overconcentration in U.S. stocks after a decade of dominance

- Fiscal tailwinds abroad from higher deficit spending and new trade agreements

- More attractive valuations (U.S. stocks trade around 22x earnings versus ~15x for developed international markets)

To be clear, the U.S. still holds meaningful advantages, including higher revenue growth and stronger profit margins. That’s why our takeaway isn’t “U.S. versus international,” but rather “good returns globally.” The past decade was an extremely one-sided story in favor of the U.S., and only recently has leadership begun to broaden. Many professionals argue that international stocks still have catching up to do—and perhaps this is simply a reminder that even market dynasties have off seasons.

Conclusion

While the news can feel unsettling at times, the bigger picture still offers plenty of opportunity. Recently, Tom Lee, Chief Investment Officer at FundStrat, made a compelling point on Compound and Friends (Episode 227). He noted that financial markets have endured an extraordinary series of challenges over the past six years.

Supply chains were rebuilt post-COVID. Consumers and companies adapted to high inflation. Businesses weathered the fastest interest rate-hiking cycle in history. And geopolitics threw just about everything—short of the kitchen sink—into corporate planning.

Lee argues that an economy and corporate sector that can continue to grow through all of that likely deserves a higher valuation multiple. Maybe the market is simply recognizing how resilient this “team” really is.

If the global economy were heading into the Super Bowl, it would be a team that battled the toughest opponents and still found a way to win. That’s not a guarantee that challenges aren’t ahead—but it is a reminder that this team has proven it can take a hit and keep moving forward. That’s a team I’d be comfortable betting on.

As always, we’re here to answer questions and help keep the focus on what’s actually driving markets.

Jordan Kaufman

Chief Investment Officer

Green Ridge Wealth Planning

Disclosure:

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment/tax advice. The investment/tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment/tax strategy for his or her own particular situation before making any investment decision(s). You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning, LLC, and are only for general informational purposes as of the date indicated.