Tax-Loss Harvesting: What is it & how do we use it at Green Ridge?

Vanguard wrote a research brief in June of 2020 that attempted to quantify the value a financial advisor might bring to a relationship. They found that working with an adviser can add about 3% value in the form of net returns, and a quarter of that value was in tax-loss harvesting. This is an often-overlooked place of value.

Below, we explain what tax loss harvesting is and its benefits to clients, as well as shine light on how we do it a little differently and what we consider best practices.

What is Tax-Loss Harvesting?

Tax-loss harvesting is a strategy used to minimize future tax impacts by selling investments that have declined in value. You are realizing the loss and turning it into a tax asset for future use. This can be used for the future benefit of offsetting potential gains or used as a tax deduction within the calendar year. There is an important consideration which is crucial to this strategy: the wash sale rule. The wash sale rule would disallow the loss to be used as a future benefit if you were to repurchase the same or substantially identical investment within 30 days of the sale date. You can avoid this by buying a similar investment. A good example of this is selling Coca-Cola (KO) and buying Pepsi (PEP), this would not trigger the wash sale rule. After the 30 days if you really love Coca-Cola (KO) stock you can buy back into it without triggering the wash sale rule.

The Benefit

There is no longer a limit on how long you carry forward losses. They can be applied to future years until the losses are used up, whether from offsetting future gains or as an annual tax deduction of $3,000.

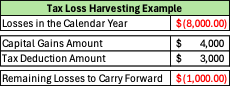

- Offsetting Future Gains: In a year where you have capital gains you can use previous years’ capital losses to offset these gains.

- Income Tax Deduction Annual Limit: You can also apply up to $3,000 of losses to offset ordinary income in current and future tax years.

As an example, you have $8,000 in realized losses in a specific year. You can use these losses to offset the capital gains of $4,000 the next year and also use $3,000 as an income tax deduction. This leaves you with $1,000 in losses that can be carried forward to a future year.

Green Ridge Philosophy

Tax-loss harvesting is a recognized strategy usually employed at year-end to help minimize potential tax impacts in future years. However, an important difference in how we think about tax-loss harvesting is that we employ this strategy year-round, whenever opportunities present themselves. As noted, advisors typically wait until year-end to do all their tax-loss harvesting, but is the end of the year really the best time to do this? Investments fluctuate throughout the year, so, at Green Ridge, we believe that proactively looking for opportunities to sell when the time is right and to capture the greatest tax-loss makes the most sense.

If you are not incorporating tax-loss harvesting in your current plan, give us a call and we will help you devise a strategy that works for you!

Appendix

See the following link for more tax information: https://taxfoundation.org/data/all/federal/2024-tax-brackets/

*In the Vanguard paper, Ordinary Income is defined as “Any income earned by an individual and is taxable at their marginal tax rate.” Capital gains is defined as “Capital gains are when you sell a stock or holding.” Further, ““a. Short-Term Capital Gains will be taxed as ordinary income, b. b. Long-Term Capital Gains have a preferential tax treatment and is lower than the ordinary income tax brackets, and c. You qualify for this if you hold a stock for longer than one year.”

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment / tax advice. The investment / tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment / tax strategy for his or her own particular situation before making any investment decision. You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning, LLC, and are only for general informational purposes as of the date indicated.