In the 1999 box office hit “The Matrix”, Morpheus asked our hero Neo to make a choice; “You take the blue pill, the story ends, you wake up in your bed and believe whatever you want to believe. You take the red pill, you stay in Wonderland, and I show you how deep the rabbit hole goes.” I feel like the dichotomy in today’s market is somewhat like the choice Neo faced; parts of the market are stuck in the traditional rules of economics and market valuation, while another part of the market is focused on a super-cycle of Artificial Intelligence (AI) driving investment and economic activity in almost every industry.

Markets are dynamic places where people commit hard-earned money to what they believe. Equity investors are skipping over the complexity of trade deals and Big Beautiful Bills and going straight to the red pill AI story. The opportunities are so great, and the risk of missing them seems higher than the risk of capital loss. On the other side, the bond market and slower growth stocks feel more blue pill, worried about the latest weak jobs number report, impacts of tariffs on margins and growth, and possible spiraling in national debt.

Quick Market Update

- S&P 500: +8.5%, up 2.4% in July

- MSCI ACWI ex-US: +18%, down 0.4% in July

- Nasdaq 100: +10.5%, up 3.3% in July

- Bloomberg US Aggregate Bond Index: +3.75%, down 0.2% in July

- Gold: +24%, down 1.5% in July

- US Dollar / Euro: -10.2%, up over 3% in July

- Source: YCharts (YTD as of 7/31/2025)

US markets and the US Dollar rallied on stronger-than-expected economic data and the Federal Reserve’s decision to keep interest rates unchanged. Mixed in there was some trade talk confusion, but that will likely be a topic in coming months as fallout from tariff policy is felt. Obviously, the passing of the Big Beautiful Bill in early July had some impact as investors digested short-term gains from lower taxes versus long-term deficits – it is estimated that the impact of the bill’s policies will grow the deficit $3.4 trillion over 10 years.

Key Themes Driving the Market

1. The AI Boom Keeps Booming

Big tech was expected to spend $325B on AI-related capital expenditures in 2025. That number has jumped to $365B. Earlier in the year, questions existed as to whether this level of investment was sustainable, especially after DeepSeek in China claimed breakthroughs in power-efficient models. But those doubts have faded as spending accelerates.

It is worth noting just how much Capital Expenditures have grown at the large tech companies. Below is a chart of the 12-month forward expectations in sales versus the forward expectations in capital expenditures at Alphabet, Amazon, Meta, Microsoft, and Oracle. You can see how sales expectations shot up from 2023 into 2024 and then flattened through 2024. At the same time, sales growth expectations were flattening, and Cap Ex growth started to skyrocket. This is why Nvidia’s stock did so well in 2024. The growth in Cap Ex grew over $100B in less than a year! We now see sales expectations turning back up again.

Source: https://sherwood.news/markets/these-two-charts-on-the-ai-spending-boom-have-something-for-everyone/

However, we should keep in mind, this isn’t just a tech story. Utilities are expected to have a growth wave due to the energy needs of AI computing. Industrial companies’ activity is also expected to see a boost to help build out the AI infrastructure, from HVAC manufacturers to cool hot servers to diversified industrials, which provide large-scale systems for energy management and hardware production. A number of real estate companies are surging with the expanded need for cloud hosting, storage, and leasing to tech companies for data centers. AI is shaping up to be a cross-sector driver, with implications across infrastructure, industrials, and technology.

So, are you wondering why markets remain strong despite tariffs, Fed drama, and geopolitical risks? I’m a big believer in Occam’s Razor; AI may be the simplest and cleanest explanation.

2. Tariffs Risk Spoiling the Party

Tariffs have re-entered center stage, largely due to an aggressive trade policy by the Trump administration. While tariffs themselves aren’t new, what is different now is the scale, the speed, and the push to close loopholes, like trans-shipping.

On what Trump deemed “Liberation Day” this past April, he announced sweeping global tariffs starting at 10%, with a plan for reciprocal rates. The market dropped sharply on this announcement, and investors panicked at the thought of a global trade freeze. The administration responded to the decline, delaying implementation for 90 and then 120 days. The cycle of shock and delay has led to a V-shaped recovery in equities.

It is also important to note that the estimated rate of inflation in the US has come down significantly since the initial announcement in April. Expectations are now almost half as low with announcements through July 27th. The chart below gives context to where we were, where we are, what we were scared of in April, and where we now think things are headed.

Source: https://www.schwab.com/learn/story/tariffs-is-worst-behind-or-ahead-us

Investors must keep in mind that only 14% of the US GDP is attributed to imports. Therefore, while these tariffs will likely hurt consumer spending power or company margins, it may not be as great as some market pundits have suggested. Certain companies will be more impacted than others, and the market is sorting that out currently.

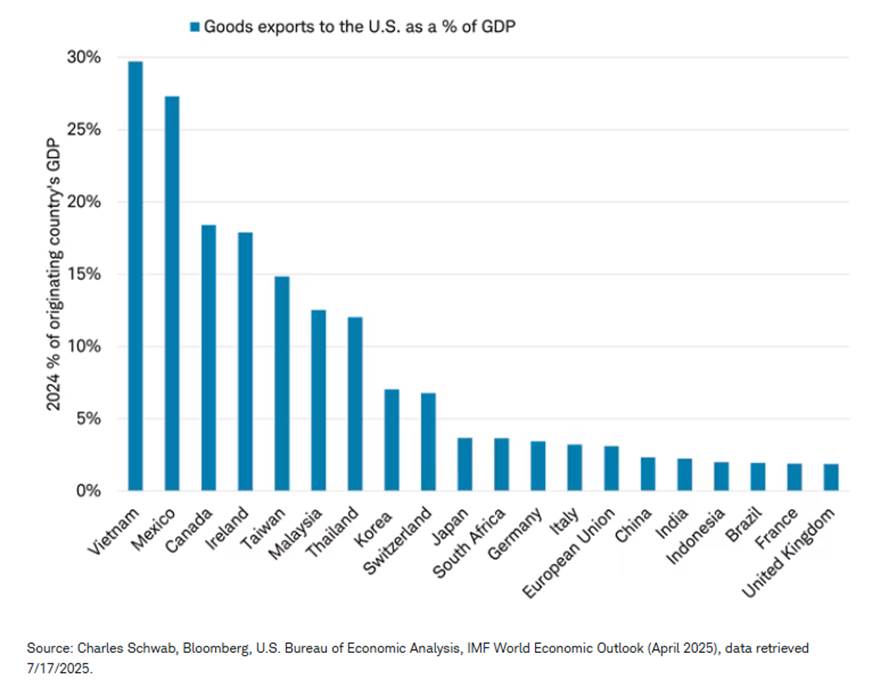

Further, only five countries have more than 14% of their GDP as exports to the US. So, while these headlines sound scary, it seems like it will be more of a short-term cycle than full-blown crisis.

Source: https://www.schwab.com/learn/story/tariffs-is-worst-behind-or-ahead-us

The impact on markets and margins has been muted thus far, possibly due to preemptive inventory building. Still, with consumers stretched from past inflation and high interest rates, the risk of inflation re-acceleration and slowing GDP is very real.

3. Federal Reserve Drama

Chair Jerome Powell and President Trump have been sparring publicly, with Trump pushing for rate cuts and Powell emphasizing data dependence. The Fed is holding off on cuts for now due to persistent inflation (~2.7%) and strong labor market data (although the announcement on August 1 showed some unexpected weakness, but this commentary is through July 31, so we won’t get into that now).

- Source: https://www.cbsnews.com/news/federal-reserve-powell-trump-fomc-interest-rate-meeting-july-30/

Trump’s pressure raises concerns about the Fed’s independence. Part of the trust the market puts into central banks is that they will not act politically, and this is something markets don’t take lightly. When countries start using independent institutions as political tools, that is when the world stops trusting data—China is a great example. This is a dangerous path, and Trump firing the Bureau of Labor and Statistics Commissioner last Friday does not help promote institutional independence. That said, this isn’t completely unprecedented; past presidents like Johnson and Nixon also were accused of trying to influence Fed policy.

Globally, other central banks are cutting rates. The European Central Bank, for example, has dropped rates from 4% to 2% since June 2024. While their inflation and growth outlooks differ, the directional shift is worth watching.

It is also notable that two Fed members dissented in July in favor of a rate cut—an uncommon move that signals growing internal debate. Keep in mind that the Federal Open Markets Committee (FOMC) Chair, Jerome Powell, does not “decide” interest rate policy; the FOMC, a 12-person committee, all vote on the policy. Even if Powell were replaced tomorrow, it is unlikely a new Chair could overcome all the different opinions on the committee.

Conclusion: Balance the Red and the Blue

At the end of the Matrix trilogy, man and machine realize they need each other to survive. That’s not far off from today’s market. On one side, we have classic valuation and cycle awareness: the blue pill. On the other, the excitement and disruption of AI: the red pill.

We saw during the dot-com era how expectations can outpace reality. While red pill investing may be thrilling, don’t abandon the discipline of the blue pill. We are very optimistic about what great innovation the future holds, but also want to be realistic about the challenges of change. Progress won’t be instant, and risk still matters.

Enjoy the rest of your summer,

Jordan Kaufman, CFA, CFP®

Chief Investment Officer

Green Ridge Wealth Planning

Disclosure:

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment/tax advice. The investment/tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment/tax strategy for his or her own particular situation before making any investment decision(s). You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning, LLC, and are only for general informational purposes as of the date indicated.