It feels like we blinked and it is already 2026!

2025 was a great year for both stocks and bonds. Often investors start asking, “Okay, what’s the catch?” It was a good year, there’s no catch!

- S&P 500 +17.9%

- Nasdaq Composite +21.1%

- MSCI All World ex US +32.3%

- Bloomberg US Aggregate +7.3%

- Source: YCharts (YTD as of 12/31/2025)

These are some very strong numbers, especially when we consider that 2023 and 2024 were also both strong years. Before we talk about the future, I feel like it is worth recapping what the heck happened in 2025. My head is still spinning from the nonstop blitzkrieg of news we just experienced. To best analyze markets, we must sift through the noise and find the real performance drivers. Below is a quick quarterly recap of 2025 (with S&P 500 returns) highlighting the themes that drove markets, and to check in for sanity’s sake:

Q1 2025: The Policy Shock (-4.3%)

- Tariff Turbulence: Initial excitement turned to fear as the administration threatened and then implemented tariffs on China, Mexico, and Canada. This sparked trade war concerns, a significant drop in the dollar, and fears of a U.S. recession by March.

- AI “Sputnik” Moment: DeepSeek’s release of the R1 model showed energy and computing power efficiencies that created questions around Artificial Intelligence (AI) economics.

- Fiscal Tightening: The Department of Government Efficiency (DOGE) began operations, signaling reduced government spending just as tariff anxieties peaked. (Because why have one stressor when you can have two?)

Q2 2025: The “V-Shape” Rebound (+10.5%)

- Policy Pause & Recovery: A chaotic implementation of global tariffs (“Liberation Day”) led to a sharp sell-off. The Administration then made a 90-day pause one week later. Markets bottomed and surged, interpreting the pause as a sign that the administration would not tolerate a prolonged equity crash.

- Fundamentals Over Fear: Attention shifted from the White House to Wall Street as the “Magnificent 7” reported blockbuster earnings, helping fuel the AI trade and promoting the idea that there would be real profits.

Q3 2025: The Pivot & The Bill (+8.2%)

- Fiscal Stimulus: The passage of the “Big Beautiful Bill” extended previous tax cuts and introduced new incentives for corporate capital expenditures, fueling business investment.

- The Fed Pivot: Following a weak jobs report in August, the Federal Reserve cut rates by 25 basis points in September, officially signaling the start of a cutting cycle.

Q4 2025: The Soft Landing (+2.3%)

- Trading in the Dark: A government shutdown in October halted economic data releases. Investors treated “no news as good news,” relying on strong tech earnings and AI infrastructure spending to push markets higher.

- Fed Commitment: Despite the data blackout, the Fed cut rates twice more (October and December), bringing them below 4%.

- Economic Resilience: Post-shutdown data showed cooling inflation and a resilient consumer, prompting the Fed to upgrade its 2026 GDP forecast to 2.3% from 1.8%.

We think the most important market movers for the year were artificial intelligence, the tariff policy, and Federal Reserve interest rate policy. There were several other things happening, but these are the things we feel are the focus looking forward.

What Can We Expect in 2026?!?!

Around year-end, big firms release outlooks, and I spend the holidays doing what everyone else does; relaxing, recharging, and reading 60-page PDFs like they were beach novels. The dominant theme this year—AI CapEx (Capital Expenditures) spend!

BlackRock’s Global Outlook claims that global AI investment could reach 5 to 8 TRILLION dollars by 2030. They highlight this as an “investment cycle”, not a “tech rally”. In my interpretation, BlackRock seems more confident in the continued success and earnings from AI than JP Morgan’s outlook, which is a little more concerned about earnings durability.

Said differently: one is saying “this is highways and electricity,” the other is saying “cool—show me the toll revenue.” Let’s go to the charts!

Earnings:

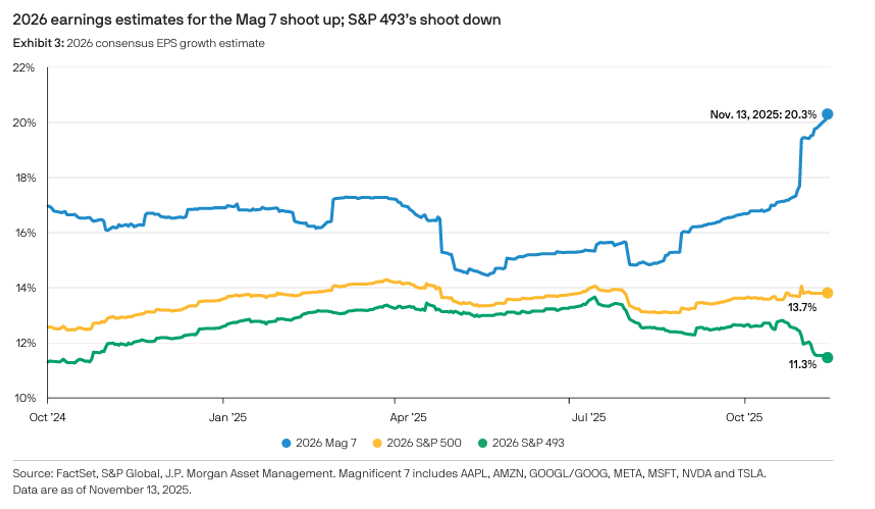

The EPS (Earnings Per Share) picture tells you everything about this market’s vibe: it’s strong… but concentrated.

Earnings expectations for the Magnificent 7 keep rising, mostly tied to AI-driven revenue and margins. Meanwhile, the rest of the S&P 500 is flat or declining.

The index can look sturdy, even while a big chunk of stocks is basically doing the financial equivalent of shrugging.

This divergence explains why market-cap-weighted indexes can keep floating even as breadth looks weak: the heavyweight lifters are still lifting.

Earnings growth is not a U.S. phenomenon.

This chart challenges the idea that the U.S. is the only place where earnings are growing. Over this cycle, earnings growth outside the U.S. —excluding China— has largely kept pace with U.S. companies when measured in local currency terms. Markets like Japan, Europe, and especially India have seen a steady recovery in profits since the post-pandemic downturn, and consensus estimates suggest that trend continues. China stands out as the clear laggard, but the broader takeaway is that global earnings growth is more balanced than recent market performance would suggest, even if U.S. stocks have captured a disproportionate share of investor attention.

Translation: the world is doing more than just watching the U.S. do AI.

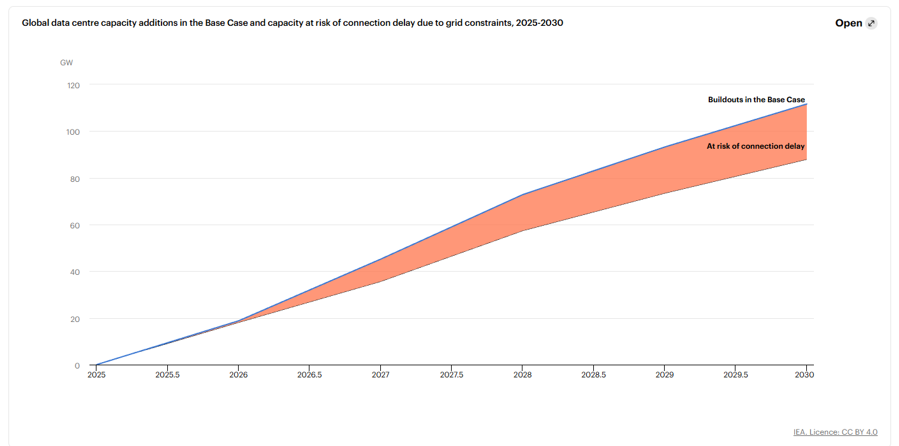

Artificial intelligence “We’re gonna need a bigger grid…..”

One of the most underappreciated risks in the AI investment cycle is power consumption. Data centers can get built quickly; grid connections… cannot. Demand for computing is accelerating faster than electrical infrastructure can keep up.

AI is no longer just a software story—it’s a “please call your local utility” story.

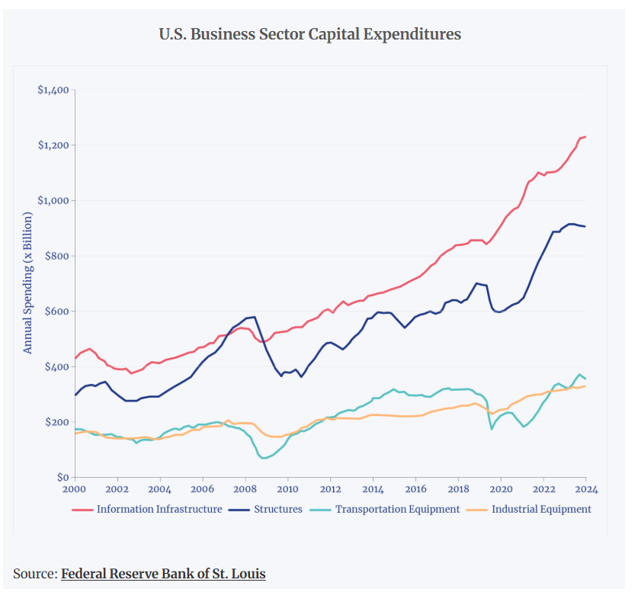

AI is reshaping the real economy. Data center construction is now rivaling (and sometimes surpassing) office construction. This supports the view that AI is capital-intensive infrastructure.

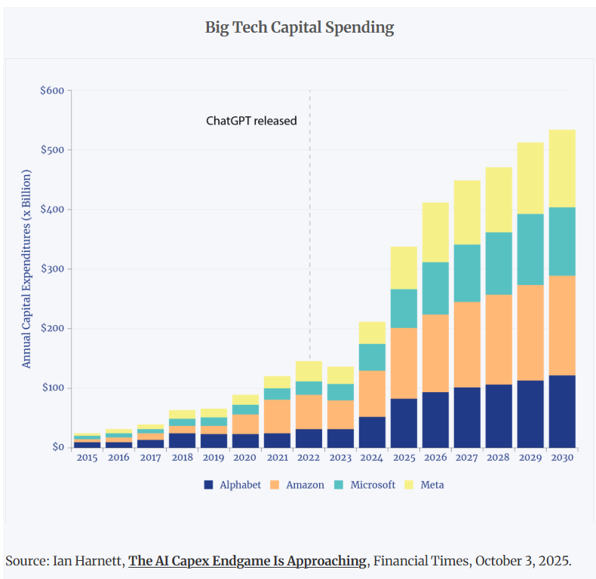

Since ChatGPT, Big Tech capex has surged and is projected to more than double over the next several years. BlackRock’s “investment cycle” framing fits here. But as spending rises, markets will demand proof that this becomes durable earnings.

In other words: “We loved the trailer. Now we need the movie.”

Information infrastructure spending (data centers, software, computing equipment) has surged to record levels, outpacing traditional categories like industrial equipment and transportation. AI capex is now one of the major engines of business spending.

- The upside: it can help support growth.

- The risk: it concentrates the economy—and the market narrative—around one very large theme.

Inflation: Tariffs to the left of me, AI builds to the right, here I am, stuck above target with you!

- Skepticism over November data: Several economists and think tanks, including those at Oxford Economics and Capital Economics, cautioned that the reported sharp slowdown in the November annual inflation rate to 2.7% (and core inflation to 2.6%) might be an anomaly due to data collection issues caused by a recent government shutdown.

- Sticky inflation concerns: Many experts believe that while overall inflation is down from its 2022 peak, the “last phase of disinflation could prove the most challenging”. The last mile of disinflation could be the hardest, leaving core inflation above target longer than investors hope.

- Impact of tariffs: The Congressional Budget Office (CBO) cited higher import tariffs as a key factor putting upward pressure on the cost of goods and inputs to production, which is expected to keep inflation elevated in the near term. They project the effects of these tariffs to peak in early 2026 before receding.

- Outlook for 2026: Projections for 2026 generally forecast inflation will ease but remain slightly above the Fed’s 2% target.

- The CBO projects personal consumption expenditure (PCE) inflation to fall from 3.1% in 2025 to 2.4% in 2026.

- Some analysts are concerned about an under-appreciated risk of AI-driven inflation in 2026, due to potential supply bottlenecks in chips and electricity from the tech investment boom.

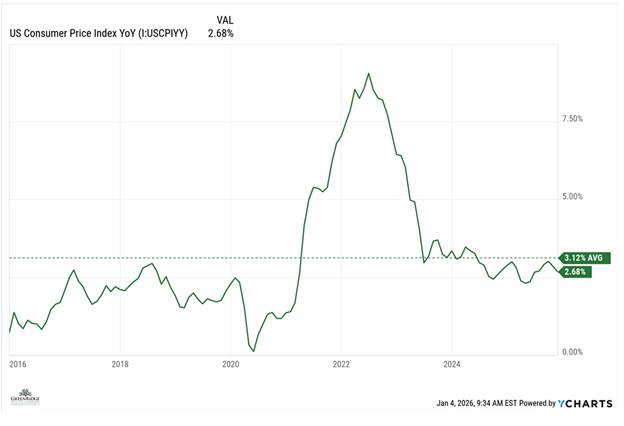

Below is a chart of the Consumer Price Index (CPI) over the past 10 years. I think it illustrates where inflation used to be before we had the paradigm shift following COVID and the invasion of Ukraine.

For interest rates, inflation seems to be open to interpretation. It is not “low”, but it is also not a major threat if you look at it objectively. With the pressure from the administration and a likely new Federal Reserve Chair in May, the Federal Reserve is likely to continue cutting rates in 2026. The issue the market has to digest is whether longer-term rates, like the 10-year and mortgage rates for home buyers, will come down with the Federal Reserve cuts. Historically speaking, 4% interest rates on the 10-year treasury are not high, and with government debt where it is, there is an argument to be made for longer-term interest rates to remain higher.

Diversification: Becoming a Stranger Thing…..

With the Stranger Things finale behind us, the new upside-down is diversification. It used to be (half a lifetime ago) that diversification was pretty simple; buy long-dated government bonds and stocks in defensive sectors to try and reduce risk.

Now AI is driving the ship, and investors are starting to understand that AI is going to impact almost everything. In their 2026 outlook, BlackRock highlighted that equity factors are starting to converge to U.S. AI news. AI drives future growth prospects, energy consumption expectations, productivity improvements, and inflation expectations. These factors have varying effects on bond pricing, Federal Reserve actions, utilities, inflation expectations……AI is Kevin Bacon in the game six degrees to Kevin Bacon! (If you don’t know that game, you should Google it….it used to be how us old people passed the time on long car rides before cell phones).

For allocating portfolios, diversification these days means finding investments that have as little to do with the AI trade as possible. This is not as easy as you would think, and traditional forms of diversification will not work like they used to. We think investors need to look for investments that have an even bigger story driving their price action to diversify away, and those opportunities are not hiding in the regular spots where asset allocators typically look.

BlackRock’s outlook for 2026 comes down to a simple idea: markets are being driven by a handful of massive forces, with AI investment at the center. The scale of spending is large enough to support growth and earnings even as the economy cools elsewhere, keeping U.S. equities well supported. At the same time, the need to finance that spending is pushing leverage higher and making interest rates more volatile, reducing the diversification benefit of long-dated bonds. In this environment, returns are increasingly concentrated, and diversification works less by spreading exposure and more by deliberately choosing where to take risks.

J.P. Morgan’s 2026 outlook highlights just how concentrated today’s market has become, with the majority of returns tied to a small group of AI-related companies. While they don’t question the transformative potential of AI, they do question whether the enormous investment underway will translate into sustained profits quickly enough to justify current expectations. Power constraints, geopolitical risks, and the sheer scale of capital spending mean that volatility is likely to remain elevated. In this environment, markets can still move higher, but leadership is narrow, pullbacks are likely and returns depend more on execution than enthusiasm.

To Sum It All Up:

Last year, AI proved to be the 800-pound gorilla for investors. We think 2026 is shaping up to have that same main character driving markets. That being said, the main character has some new challenges in the sequel. We are pressed up against real-world challenges like energy constraints, building timelines, and real earnings. It is easier to see the potential of new technology than it is for the technology to become a reality.

We look forward to seeing how things evolve, but we expect it to be an exciting story that smart investors will navigate thoughtfully.

Wishing everyone a happy and healthy new year!

Jordan Kaufman

Chief Investment Officer

Green Ridge Wealth Planning

References:

- BlackRock Investment Institute: 2026 Global Outlook, Pushing limits

- J.P.Morgan: Eye on The Market | Outlook 2026, Smothering Heights

Disclosure:

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment/tax advice. The investment/tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment/tax strategy for his or her own particular situation before making any investment decision(s). You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning, LLC, and are only for general informational purposes as of the date indicated.