November Commentary

The election is over, and that means we might finally stop receiving text messages for political donations! Over the next month, we will have a better idea of what the impact of the election will be on the markets, so we will save that discussion for our December commentary. In the meantime, let’s look at some of the key issues that can sometimes be drowned out by politics.

- Corporate Earnings: Earnings have been growing well for over a year now. While growth in earnings is starting to slow, things still look to be pointing in the right direction.

- The Economy: The U.S. economy continues to grow at a healthy clip. While U.S. employment numbers are starting to raise slowdown concerns, there is some optimism that global growth may pick up.

- Inflation: Since inflation has come down globally, central banks are feeling much more comfortable that it is under control. That being said, prices remain high, and economists will continue to monitor inflation closely as new policies may cause prices to rise again.

- Central Banks: With inflation way down in the past two years, central banks globally are starting to ease overnight bank borrowing, helping to stimulate economic growth.

- Long-Term Interest Rates: While short-term borrowing rates are dropping, longer-term bond rates have recently started to rise. Expectations of increased global growth are the most plausible reason for this shift.

So, while we don’t yet know what the impact of the election will be, the economy, inflation, and central bank activities are pointing to continued growth for the markets. Despite both the economy and markets being on a much shakier footing than they were eight or twelve months ago, we must keep our eyes on how things might shift with fiscal policies, monetary policies, and global uncertainty. And that is why we are here!

Let’s dive into the issues mentioned above in a little more detail.

As we have highlighted in past commentaries, corporate earnings have really been doing most of the talking. As I write this, ~70% of companies in the S&P 500 have reported earnings for the third quarter 2024. The year-over-year earnings growth rate is about 5.1%, and the blended revenue growth rate is 5.2% (according to FactSet, a trusted financial data and analysis system for financial professionals). These numbers are solid, and while it is a slight decline in growth from some of the past quarters, it is a far cry from a recession, which is where some feared we were headed at the end of the summer. Earnings have grown for five consecutive quarters, and revenue has grown for sixteen consecutive quarters.

Not all sectors are benefiting the same. In the last month, Energy, Industrials, and Health Care sectors have lowered their Q4 earnings estimates looking forward, while Communication Services and Financials have raised their estimates.

It is amazing how the big corporate juggernauts impact the data. For instance, Alphabet (Google) and Meta (Facebook) had huge positive impacts on the growth in the Communications sector. The sector showed a quarter growth of 21.7%! However, if you “x” out the numbers from Alphabet and Meta, the growth rate drops to 7.3%.

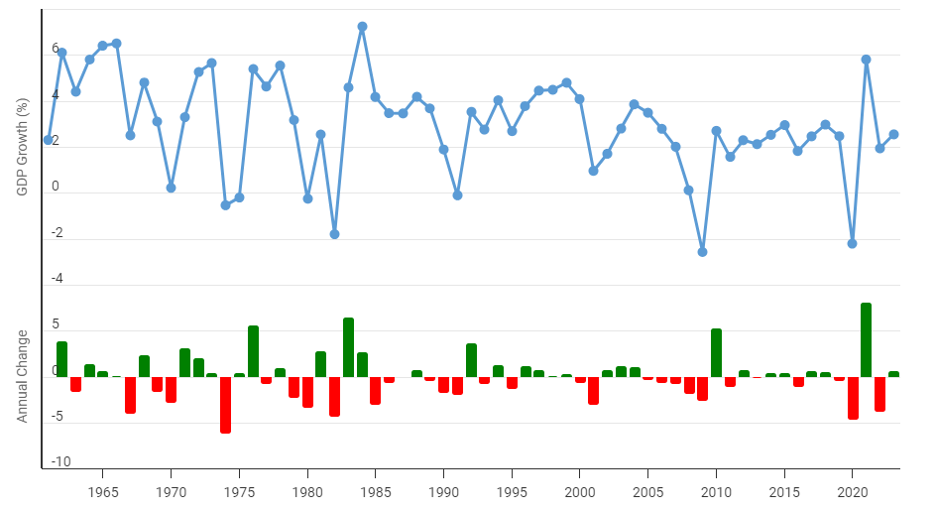

U.S. GDP grew 2.8% in Q3. If we look at developed economies, the average GDP growth is around 1.8% in contrast. Average GDP growth for the U.S. has been 3.2% over the last eighty years. In the chart below, which highlights eighty years of GDP growth (quarterly), we can see that the U.S. economy is less cyclical, but the declines are sharper and deeper when they occur. Market data reflects the same characteristics. This also makes sense when we look at the company and business mix in the U.S. and how it has shifted in the last eighty years from manufacturing to more technology and services. This also helps explain why we recovered so quickly after the COVID crisis as compared to the rest of the world.

Source: macrotrends.net

The Federal Reserve cut interest rates on the overnight-lending rate by half of one percent in its September meeting. The current market predicts it will cut interest rates again in the November meeting. Except for the Japanese Central Bank, almost all major central banks around the world have been cutting interest rates or pointing towards cutting interest rates. Central banks are scaling back their restrictive monetary policy as they feel the major inflation threats are subsiding.

In October, the 10-year U.S. Treasury Bond Yield moved from 3.75% to 4.3%. This is a monster increase in rates, and many people have been speculating as to why. Because American journalists sometimes forget we live in a global economy, many pointed to the election and assumed outcomes as the driver. But if we look at the yield on 10-year Euro bonds, we see the same kind of movement, from 2.0% to 2.4%. Around the same time there was a big fiscal announcement for economic stimulus in China. If we really look at the move in yields globally, it seems to be more optimistic about growth going forward on support from central banks.

We recognize there is a lot to digest. As we always do, we will keep our eyes on things and make sure we are factoring in the environment and necessary changes in real time, so you don’t have to worry about it. Happy Thanksgiving to all!

Jordan Kaufman

Chief Investment Officer

Green Ridge Wealth Planning