“Drinks on Me!” We are mere humans, so when we get a big raise, bonus, or are feeling flush with cash, we want to spend! Some of that desire is to reward ourselves. Some of it is to let those around us know that “we made it!” The problem is that it is hard to identify when you have gone too far and now you are overspending.

What is “Lifestyle Creep”?

Lifestyle creep is when you spend more as you earn more. Also called lifestyle inflation, it is a normal process where you live according to how you perceive you should be living based on how you feel about your income. When we are poor college students, we all eat pizza, drink cheap beer, and sleep on futons. As we become professionals, we start to look through furniture catalogs and get snobby about what car we drive.

Even with the best intentions, the problem occurs when our income growth starts to slow down, and real expenses continue to ramp up. Bigger houses have bigger maintenance expenses. As our families grow, so do our expenses. And even if we just think about budgeting for a trip, we often forget to include the uber to and from the airport and the $5 water we buy when we get to the airport.

The thing we need to keep in mind with lifestyle creep is that it does not matter how much you make; you can spend more than you earn. As an advisor, too often we see situations where people make 6 or even 7 figures and still somehow spend more than they make.

Below are some tips to help those with growing incomes to make sure they are also growing wealth.

Keep a Budget:

So easy, yet so hard. You want to make sure you are not overeating, start calorie counting. You want to make sure you are not overspending, keep a budget. Yes, it is that easy. It’s the discipline that is hard.

Simple rule is don’t spend more than you make. If you are getting 1,000 per paycheck, try and only spend 800 – 900 per pay period. Budgets are obviously much more complicated, and some of us have necessary expenses that we can’t get around, but if you build out a plan that saves around 10% to 20% of your paycheck, you will be in better shape to handle the unexpected.

No Credit Card Debt:

This is not an option. Credit card debt is addictive. You can spend like crazy and then only have to pay a portion. It is a wonderful phenomenon that our society has made borrowing so easy, with paying on lay away and purchase incentives, but you can get yourself into some real trouble here. Pay off everything as part of your monthly budget. Don’t just pay the minimum payment; have a plan in your monthly budget to pay everything off.

The real problem is when you have interest accruing against debt. Especially with credit cards, the interest rates are often so high that you can find yourself falling way behind if you let it even get a little out of hand. Be a fanatic about getting rid of debt and keeping a lid on it.

Forced Savings:

The best way to make sure your lifestyle doesn’t creep past your income is to have forced savings. A no brainer is to put money into a 401k each pay period if it is available to you. But another important step is to get in the habit of saving a portion of each paycheck into a brokerage or savings account. Making a percentage, and a good benchmark is 10% of each paycheck. This way if your income goes up, your savings will go up proportionally.

The Short and Sweet of it:

As we climb the corporate and earnings ladder, we want to reward ourselves for the hard work. And we encourage this! But don’t forget to follow a few simple steps to make sure your lifestyle creep doesn’t creep its way into destroying your bigger goals.

Keep score on your spending versus your income, and make sure you are in the net positive. Don’t carry any unnecessary debt that has high interest rates. And make sure you are saving a portion of every paycheck.

Follow these rules you’ll have mad bread to break up!

10 Keys to Prepare Your Business for Sale

Your business is more than likely one of your biggest, if not THE biggest, asset you have. The better organized and prepared you are in your business, the higher value you can demand. That means your thought process around a sale starts right now, even if you don't plan to sell for years. Consider the following points to be keys necessary for having a successful transaction when the time comes for you to sell your business as well as a way to ensure you get the most value out of your sale.

Be Ready to Sell at All Times

"But I'm not ready to sell!" Having the mindset to be ready to sell at any time, but run it as long as you need, allows you to have the processes in place that potential buyers will pay top dollar for. Fixing things before a sale pokes holes into the organization that you don't necessarily notice until you go through the process. And, trust me, the buyer will notice one way or another in their due diligence. Arguably the most important point in this entire blog, make sure you can easily be replaced. If your business cannot operate without you, it is far from a flourishing organization which will hinder your ability to sell.

Communicate Your Vision of the Future

Buyers will price your business on past performance and trends, but your vision of the future will allow more context to the buyer for what it is they are buying. Finding synergy for the buyer, not making them look for ways to justify their purchase, puts you in the driver’s seat. This will avoid any grey areas in potential buyers’ minds as to what they are purchasing for the price they are willing to pay.

Understand Your Business Value & Value Drivers

More often than not, business owners feel that certain things they do or don't do will affect their value, when in fact, it may not at all. What that results in is wasted time and dollars toward the wrong initiatives that do not provide the intended increase in value.

Avoid Surprises through Self-Due Diligence

All buyers willing to engage in the transaction of your business are going to do detailed due diligence and research into the business they are considering for purchase. Most buyers even hire or outsource professional due-diligence teams to verify representations and find any concerns or discrepancies that may be present from a value-add perspective. You can avoid any surprises and ensure a smooth transaction by staying ahead of your potential buyers in doing your own due diligence. Overall, many of the last-minute issues that arise during mergers/acquisitions are unbeknownst to the business owner.

Address Customer & Supplier Concentration

Customer concentration and supplier concentration are the two main areas of risk that can affect business continuity from the perspectives of potential buyers. Having a business that is dependent on a select number of customers or suppliers will negatively affect the valuation of your company. Wherever and whenever possible, be sure you are trying to find ways to diversify your customer and supplier base to mitigate these risks. The moral of the story is that big clients are great, just make sure only a small group of them make up the majority of your business.

Lock in Key Employees

Another area where risk arises for potential buyers is your company’s dependency on a few key players or employees. Most buyers do not operate their new business with the intention of firing employees in hope of saving cost, they look to retain key talent. They also want to make sure key talent doesn’t walk away with trade secrets or clients. So, they want sellers to focus on employee retention and retaining leadership. By locking in key employees through different tools like non-competes and non-solicitations ahead of time, you can ensure a smooth transition as well as a stronger valuation when the time comes to sell your business.

Prepare Supportable Financials

Potential buyers must have absolute confidence in the accuracy and transparency of the financial representations you make regarding your business. Further, they will most likely come equipped with a team of financial due-diligence analysts when the time comes for them to consider the purchase of your business seriously. The overall quality and impenetrableness of your financials will play a key role in the valuation of your business and solidification of your transaction. Be sure that your financial statements are reliable, accurate, and available in a timely and organized fashion.

Optimize Working Capital, Don’t Leave Money on the Table

You would be surprised how many business owners leave money on the table when selling their businesses because of their lack of understanding or ability to manage working capital. Surprisingly, you can significantly increase the value of your company by reducing its current assets. Having your money working for you through reinvestment, growth and development will increase the value of your company from the perspective of business succession.

It’s What You Keep That Counts

When finally approaching the time of transfer, it can become easy to misconstrue the value you are walking away with after lots of large numbers are brought to the table. The true value of the transaction lies in the after-tax yield of the sale, not the large number agreed upon between the buyer and seller. Meaning, it's what goes in your bank account, not what number goes on the check. It is absolutely crucial that any deal you make be structured in a tax-efficient manner. Depending on whether your firm is set up as a C-Corp, S-Corp or an LLC, you could face double taxation at the time of sale. In this step, it is also important to consider estate planning. This is why waiting until you're ready to sell to start planning can be disastrous to your outcome.

Keep Your Eye on the Ball

The most important thing to do, at the end of the day, is to keep running your business and continuing to execute on the things you have been doing. If you are preparing your continuity plan, chances are you already run a successful business that will have value to offer potential buyers. If nothing else, make sure your business keeps running efficiently and remains attractive in terms of its ability to provide value to clients/customers. The last thing a business owner wants is to neglect their business while making critical decisions like preparing for sale. This highlights the importance of hiring a team of trusted professionals to guide you through the process allowing you, the business owner, to continue the successful operations of the company.

Preparing your business for sale is not a task to tackle at the eleventh-hour; it’s a continuous journey essential to maximizing the value of your company. Further, it’s important to remain proactive in optimizing efficiencies and ensuring operational independence from yourself, the business owner. Finally, the true measure of a successful merger or acquisition is not the sale price associated with the transaction, but the after-tax yield acquired by the business owner(s) after closing. This highlights the importance of working with a team of trusted professionals whose expertise lies in the areas of tax mitigation, business succession/continuity planning, and estate planning.

Source:12 Critical Steps to Prepare Your Business for Sale -Prepared expressly for VISTAGE members. By, The DAK Group.

February CPI Report: Inflation Remains Annoyingly Stubborn

Breaking News This Morning:

February CPI Inflation rate rises to 3.2%, above expectations of 3.1%. Core CPI fell to 3.8%, above expectations of 3.7%.

“What is CPI?”, “How does it impact us?” and “Why should we care?”

CPI (Consumer Price Index) tracks the changes in the price of goods and services over the last year.

Core CPI (Consumer Price Index) tracks the changes in the price of goods and services over the last year, excluding food and energy.

It measures the price increase of goods and services, which will ultimately impact the Fed's decision to make a change in the Fed Overnight Rate, which ultimately impacts interest rates. These changes affect borrowers and savers. If you are shopping for a mortgage, you will see that rates are higher than they were. On the other hand, you'll note that your savings account interest rate is higher than it was previously.

What’s the News?

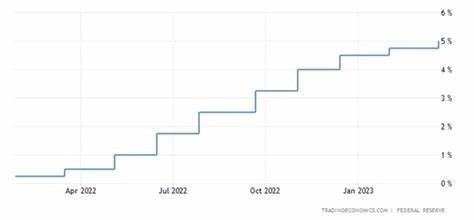

Inflation and interest rates remain a hot topic in 2024. We are now in a waiting game to see when the Fed will start adjusting rates downward. While inflation has moderated greatly from it’s peak in 2022, it remains stubborn in falling to the Federal Reserve’s target of 2% (which is a target and, quite frankly, a made up goal that has little reasoning other than it being a “goal”). The CPI release this morning marks the 35th consecutive month with inflation above 3% and the second straight increase.

The Federal Funds rate is currently in the range of 5.25% - 5.5%. The original expectation of six interest rate cuts in 2024 has swiftly dissipated, as even three rate cuts in 2024 seems optimistic in the current environment. Jamie Dimon, CEO of JPMorgan Chase said “If I were them, I would wait” in reference to the Federal Reserve cutting rates. The Federal Reserve has made it clear that they will not begin cutting rates until they are confident that inflation is heading back down towards that 2% target. With the stickiness we have seen from inflation, we would not count on a rate cut in the next few months and think interest rates being higher for a longer is a likely outcome.

This is not a great shock to what we are doing, but it gives us some guidance as to what to anticipate moving forward. We continue to monitor economic data and market trends as we make decisions in portfolios. As we always, there is no lazy asset management here at Green Ridge Wealth Planning.

Please reach out if you have any questions on the current environment or would like to touch base about your finances.

2024 Updated Tax Limitations: Top 5 Things to Know

Every year the IRS changes tax limitations to account for inflation and other economic factors. These adjustments ensure that tax-related figures like income brackets, deduction amounts, and contribution limits remain up to date and reflective of current economic environments. The top five changes for 2024 that you should be aware of surround Traditional IRAs, phase outs, Roth IRAs, company sponsored plans, and gift tax benefits.

Traditional and Roth IRA Annual Contribution Limits

With these recent adjustments by the IRS the 2024 annual contribution limit was increased by $500 to $7,000 for both Traditional and Roth IRAs, allowing individuals an enhanced opportunity to maximize their retirement savings. Last year annual contribution limits for both Traditional and Roth IRAs maxed out at $6,500 with an additional contribution of $1,000 allowed for those over the age of fifty qualifying for catch up programs.

Phase Outs

Individuals contributing to Traditional IRAs with income of $77,000 or below qualify for full deductions in 2024, and partial deductions up to $87,000. Individuals making more than $87,000 do not qualify for Traditional IRA contributions, a $5,000 increase from last year’s phase out limit of $83,000. Married individuals filing jointly with combined income below $230,000 qualify for full deduction this year while those with combined income above $240,000 do not qualify for Traditional IRA contributions, a $12,000 increase from last year.

Individuals contributing to Roth IRAs with income of $146,000 or below qualify for full deductions in 2024, and partial deductions up to $161,000. Individuals making more than $161,000 do not qualify for Roth IRA contributions, an $8,000 increase from last year’s phase out limit of $153,000. Married individuals filing jointly who contribute to Roth IRAs fall under the same phase out limitations as Traditional IRA contributors in 2024.

Company and Employer Sponsored Plans

The annual limit for tax-deferred contributions into qualified retirement plans, 401(k)s and 403(b)s, rose $500 to $23,000 this year. Maximum annual additions to SEP IRAs rose to $69,000 in 2024, up $3,000 from last year. The new maximum compensation that will be considered for SEP IRA individuals is now $345,000. Individuals over fifty years old who qualify for catch up programs are still entitled to a $3,500 additional contribution.

Gift and Estate Taxes

Annual gift exclusion tax exemptions continue to rise this year as well. A $1,000 increase from last year’s $17,000 limit now allows individuals to make charitable contributions up to $18,000 tax free annually. It is important to remember that substantiation is required for gifting, so remember to keep track of your un-taxable expenses!

If you have any questions or are interested in learning more about the 2024 tax limitation changes, please reach out to our team or check out the 2024 Tax Reference Guidehere.

January Commentary

2024 is off to the races with January coming to a close. Our monthly commentary is meant to touch upon the month’s trending news and give our perspective on “what’s happening?” and “why should we care?”. Let’s go over the few topics that have really driven headlines:

S&P 500: With still a day left to the month, S&P is up about 4%, continuing the strength from last year’s strong finish. The gain was driven mostly by strong economic data, continued lower unemployment, and lower inflation numbers (The Fed-preferred inflation gauge of PCE was lower but, CPI, the more popular number, was a bit higher). Fourth-quarter earnings are being released; results have been mixed but generally good. Some of the concerns we are hearing are focused on the upcoming election, forward looking earnings, conflict around the globe, and the high debt on both the public and private side.

Political Royal Rumble: We urge everyone not to let their political views play too much into their investing views. Trump? Haley? Biden? The market would say, “who cares?”. While the controlling powers help to write and change legislation, the makeup of the Legislative Branch bears more weight than who gets elected. Voting-politics is a money-losing strategy. Vote with your politics, invest with your intellect.

Global Conflict: Red Sea tensions have been a focus of the market for 24 months now, and while we will keep an eye on it, business has become pretty good at managing supply chains. This was tougher during Covid when supply-chain issues impacted inflation tremendously. Let’s remember, a major driver of that situation was the lack of personnel to unload the ships that did make it to the coast. While global tensions are high, the market seems to be shrugging it off. Political headlines can’t always be translated to our markets.

National Debt Crisis or Modern Monetary Theory?: Debt is an issue that is more complicated than meets the eye. We’ve said it before - for individuals and business owners, there is a difference between good debt and bad debt. We hope our elected representatives act responsibly, but this issue is likely to remain a concern for some time. The relative level of over 100% debt to GDP in the US is concerning, but keep in mind that Japan has over 200% debt to GDP. In other words, this may not be an immediate threat to the markets, but we would love to see the fiercely polar political fights simmer down and experience some sense of compromise for the American People.

Let’s see what February news brings. Wall Street Experience, Main Street Mindset!

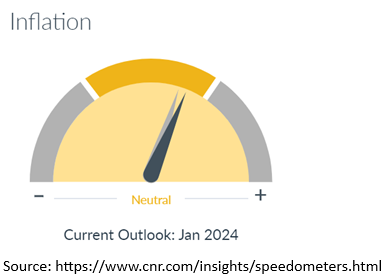

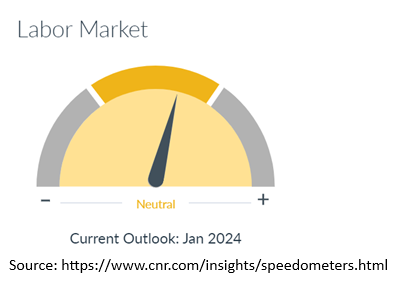

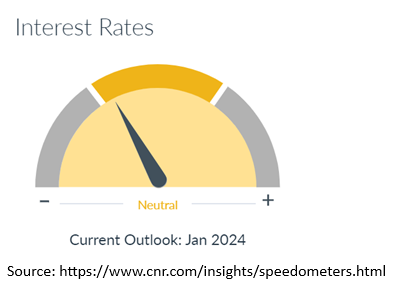

Inflation. Labor Markets. Interest Rates.

The three topics listed above each play a pivotal role in the overall health and stability of our economy and have been hotly discussed over the past few years. With the start of 2024, we want to provide you with an update on these three economic indicators and highlight what you should expect moving forward.

Overview:

Inflation has moderated tremendously since its June 2022 high. However, it remains above the Federal Reserve’s long-term target of 2%.

Labor Markets have remained extremely resilient, with unemployment rates still below 4%. With interest rates at restrictive levels, will this strong labor market endure?

Interest rates seem to have potentially reached their peak. The market is expecting a rate cut in the next few months, but don’t be surprised if rates stay at this level for longer than expected.

Inflation

Current Inflation Rate: 3.1% year over year

Next Inflation Release: January 11th, 2024 (tomorrow)

We have seen significant progress in the inflation rate over the last 18 months, from a trailing 12-month peak of 9.1% in June of 2022 to its current rate of 3.1%. This progress is part of what sparked the market rally of 2023, but the job is not yet finished as the Federal Reserve has a (arbitrary) target of 2% for inflation. Tomorrow’s CPI release for December will give us another data point, with the current expectation for inflation being 3.2%. While this would be a slight uptick, inflation does not necessarily move linearly since it is measured from the same month of the previous year. It is important to consider the movement of these data points directionally over a span of months.

We may still be off from hitting that 2% target, but we are encouraged by the drastic fall and continued downward momentum that we have seen in inflation. You can count on the federal reserve maintaining a restrictive interest rate until they are confident that the 2% target will be reached.

Labor Markets

Current Unemployment Rate: 3.7%

Next Unemployment Release: February 2nd, 2024

Labor markets have remained surprisingly strong in the face of rising interest rates, as unemployment has held between 3.4% -3.8% since the start of rate hikes in March of 2022. Higher interest rates create a restrictive economic environment which typically leads to an increase in unemployment. The fact that unemployment has remained so low through this period speaks volumes about the resilience of our economy. For some context, 3.4% is the lowest unemployment rate our country has seen in the last 54 years, so being able to hover around that number in the midst of restrictive rates has been a testament to the strength of our economy thus far.

While the labor market has held strong, rates are still at a restrictive level which will continue to put pressure on this part of the economy. Labor markets tend to be strong when there is optimism and growth on the horizon. Alternatively, when business trends are downturned or efficiencies are created through technology, businesses trim their labor expenses since it is usually one of the highest expenses on their profit and loss statement. We expect that by the end of this interest rate hiking cycle, the unemployment rate will see at least a slight uptick and may breach that 4% mark. As of now, economic data is not showing a downturn, but with company stances on work-from-home changing, we may see a softening of that number. We will be keeping a close eye on the labor market which will continue to be affected by the Federal Reserve’s approach to interest rates.

Interest Rates

Current Federal Funds Rate: 5.25-5.5%

Next Federal Reserve Meeting: January 31st, 2024

The raising of interest rates is the Federal Reserve’s main tool for combatting high levels of inflation. Over the last 2 years, the Federal Reserve has aggressively raised interest rates and has dampened the scorching hot inflation that we were seeing in 2021 and 2022 due to post-Covid supply constrains and excess dollars being injected into the economy. While great progress has been made, their final target of 2% inflation has not yet been reached. The balancing act for the Fed is to not act too early and overheat the economy again, but to also not act too late where a jumpstart is needed to reinvigorate the economy. So far, the soft landing has been more a reality than a fairy tale. However, the Fed still has to be very observant and not tip the scales.

The "Market" is showing a belief that interest rate cuts will be coming as soon as March 2024, with almost 70% estimating a reduction of the federal funds rate in that month’s meeting.

With a Federal Reserve that was slow to begin interest rate raises in 2022, and an inflation number that is still 1.1% over their target, it would not be surprising to see the Federal Funds rate remain at its current level for a larger part of 2024. This is something we will continue to monitor as we position portfolios and look to take advantage of the economic landscape.

January: Financial Wellness Month

New Years resolutions pass beyond the gyms, weight losses, dry January, forgiveness, and dedications to trying new things. January is Financial Wellness Month, and there are 5 goals you should take into this new year.

Invest in yourself – people like to talk about budgeting and savings. While those things are important, raising your income potential can be even more impactful. So, if you are looking to move up the ladder, start your own business, or grow your business, remember to invest in yourself. That can be in further education, buying a book, listening to a podcast, taking a class and getting a designation or specialty, hiring a coach or mentor, or even taking a well needed break to think, exercise, and refresh those brain cells.

Money doesn’t buy you happiness, but financial security surely brings a different level of peace into your life. Do the planning to determine what steps you need to make to become financially independent. If it is complex financial software with an advisor, or an excel spreadsheet in your pajamas, little planning is better than no planning. Do this at least once every year to keep on track with your financial independence goals!

Dollar Cost Average into your savings and Up your contributions. If it is to savings, 401k, or education, January is the time to up your monthly contributions to take advantage of moving markets. When you put a fixed amount into investments over periods of time, we call that dollar cost averaging. Meaning you are averaging the cost you buy into an investment by purchasing at different prices as opposed to trying to time the market. This is a proven method that helps novice investors to the sophisticated investors succeed over time. If you have been doing this, up your contributions by 5%, 20%, 100%, whatever you feel you can comfortably add to your savings to stay consistent and not feel the pinch of being short on money

Pay off your credit cards because interest rates are high! While we know credit card rates are generally high interest rate instruments, now that interest rates have risen they have risen too! We like using credit when credit can be managed within your budget. Buy now and pay later can cost you money that should be going into your savings and upping your contributions.

Pay attention to your cash! If you have cash that isn’t either sitting in a high yield checking, money market account, or is being dollar cost averaged into investments, you are doing your quest for financial independence an injustice and are taking the local train 20 stops as opposed to 4 stops on the express train.

“Follow these rules you’ll have mad bread to break up”

As we go into the end of the year, it is important to know what changes lie ahead so that your plan is up to date and the appropriate adjustments can be made. Below you can click on the provision to bring you to the area in the Act that is referenced.

Employers can offer a deferral-only "starter" 401(k) that automatically enrolls all eligible employees at a deferral rate of at least 3%, but no more than 15%. The deferral limit is the same as the IRA limit: $7,000 for 2024; $8,000 for those age 50 and older.

This is a simple way for small employers to set up a retirement plan for their employees that’s an alternative to state-mandated savings plans.

The beneficiary of a 529 plan can roll over money from a 529 into a Roth IRA account in their name. At the time of the distribution, the 529 must have been open for a minimum of 15 years, and the amount that’s rolled over to a Roth IRA must have been in the 529 account for at least five years. The rollover amount is limited to a lifetime total of $35,000 and is subject to the annual IRA limit ($7,000 for 2024; $8,000 for people 50 and older).1

This allows unused money in a 529 plan to be rolled over to a Roth IRA where withdrawals are tax-free. This creates a new way to benefit 529 account beneficiaries and helps reduce anxiety about unused money in a 529 account.

Employers can treat participant’s student-loan payments as an employee elective deferral for the purpose of a matching contribution to the retirement plan. These matching contributions must be made available to all participants eligible for a matching contribution.

This benefits employees who may not be able to save for retirement because they’re focused on paying down student debt. This allows them to pay down their student debt without forfeiting retirement plan contributions.

Early distributions from 401(k) plans aren’t subject to a 10% penalty if used for immediate financial needs due to personal or family emergency expenses. A distribution of up to $1,000 is permissible once per calendar year. The participant has the option to repay the distribution within 3 years, and additional emergency distributions aren’t permissible during this period unless repayment occurs.

This gives participants penalty-free access to their money to help pay for unforeseen emergency expenses.

Participants who self-certify that they experienced domestic abuse can withdraw the lesser of $10,000 (indexed for inflation) or 50% of the participant’s account. This distribution is not subject to the 10% penalty for early distributions. The participant has the opportunity to repay this withdrawn amount over 3 years, and they will be refunded any income taxes on the repaid money.

This gives domestic-abuse survivors penalty-free access to their retirement account to help pay for expenses such as escaping an unsafe situation.

Santa Rally?

Last month, our commentary focused on how pessimistic outlooks had missed some of the positives in the economy and market. What followed was a manic rise in the markets in the month of November.

November and December are historically strong months. Sometimes dubbed “the Santa rally”, we tend to see stocks drift higher into the end of the year. This is not always the case, but with some big technical reversals in the markets in the last 2 months, odds favor a rally into the new year.

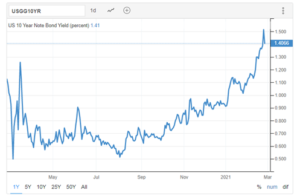

One important reversal to be aware of is in the 10-year Treasury Bond. Considered a benchmark for prevailing rates, the 10-year yield started the month at over 4.9% and ended the month close to 4.3%. That is a big decline in interest rates in a very short time!

While some of the data supports the decline in interest rates, the size of the decline is probably better described by the market's persistence on the Federal Reserve to cut interest rates in 2024, and cut them significantly! This is a reasonable assumption if we were to remove politics and sentiment from the equation; but when have politics and sentiment not been a factor!?!? The more likely outcome is that the Federal Reserve will cut rates later than they should, just like they resisted raising rates until inflation had taken a strong hold. It is likely that they will need to see either inflation below their 2% target or a significant change in the labor market and GDP growth to budge from their current interest rate target. While they may be late to cut, it also seems that the chances of another hike are remote.

“Be curious, not judgemental.” – Ted Lasso

While predicting interest rates can be fun and make for good cocktail conversation, we encourage investors to spend more time being observant. With such incredible outperformance of the top 7 largest technology stocks this year, it begs the question if that fantastic run can continue. January will be an interesting month to watch, and will likely indicate if there is going to be leadership change. Will the other 493 stocks in the S&P 500 catch up? The first month of 2024 will give a strong hint of whether or not that will be the case as institutional investors will certainly be making positioning changes. No need to guess or predict what they will do, as their ships turn slow. We will get a glimpse in January where they want to steer the boat, and our more nimble schooners can change course and pull ahead.

But enough of all this market talk and worry about the year to come. Tis the season!

Navigating the Power Struggle: ChatGPT, Sam Altman, and the Ethical Landscape of AI

Introduction:

The unfolding power struggle within OpenAI, particularly involving its flagship AI model, ChatGPT, holds profound implications for the trajectory of artificial intelligence (AI) and the delicate balance between technological advancement and human well-being. This narrative is not just a corporate saga; it is a reflection of the ethical considerations and pivotal choices we face as AI becomes increasingly integrated into our lives.

ChatGPT: A Brief Evolution and Purpose:

Launched in the past year, ChatGPT has swiftly transformed our perceptions of AI. Originating from OpenAI's ambitious mission, founded in 2015 by luminaries such as Elon Musk and Sam Altman, ChatGPT was conceived to explore AI for the betterment of humanity and to safeguard against potential risks associated with such advanced technology. What many may not be aware of is its initial non-profit orientation, later evolving into the commercialized version we encounter today.

The Functionality of ChatGPT:

ChatGPT operates as a dynamic system that translates user prompts into coherent textual outputs, effortlessly bringing thoughts to life. Its ability to generate contextually relevant responses has captivated users and opened up new possibilities in various domains.

The Dramatic Upheaval: Sam Altman's Ouster and Reinstatement:

In a surprising turn of events, Sam Altman, the co-founder and CEO of OpenAI, faced a temporary ousting from his position, sparking a dramatic series of events. The catalyst for this upheaval was the contrasting visions between Sam and the board regarding the future of ChatGPT. While Sam recognized the potential for growth through increased funding and research, the board remained steadfast in upholding the original non-profit mission — a commitment to safeguarding humanity.

Negotiations and the Resilience of Ethical Values:

Amidst the turmoil, Sam Altman received a tempting offer from Microsoft, a significant investor in OpenAI, to continue his research there. This move triggered a groundswell of support from OpenAI employees, with the threat of a mass exodus to Microsoft. Negotiations ensued, resulting in Sam's reinstatement at OpenAI. Remarkably, the board members who stood in opposition found themselves compelled to step down due to misalignment with the core mission.

Conclusion: Ethical Guardianship in AI's Future:

The saga surrounding ChatGPT and Sam Altman's reinstatement serves as a microcosm of the broader ethical considerations that underpin the development and deployment of AI. It highlights the delicate balance between commercial interests and the responsibility to protect humanity from potential risks. As we continue down the path of AI advancement, this narrative reminds us of the importance of staying true to ethical principles, even in the face of technological progress. The power struggle within OpenAI reflects a pivotal moment in the ongoing dialogue about the responsible development of AI and its implications for our collective future.

Green Ridge Wealth Planning Welcomes Jessica Lascar as Director of Marketing & Communications and Amy Early as Executive Assistant

October 25, 2023 (Montville, NJ) - Green Ridge Wealth Planning, a financial planning and investment management fiduciary, has hired Jessica Lascar as Director of Marketing & Communications and Amy Early as Executive Assistant.

Lascar joins GRWP after a hiatus from her marketing and public relations career to raise her children. Previously, she served as Public Relations Manager for Bloomingdale’s and Senior Account Executive at MWW Group (now Mike World Wide). Jessica graduated from Lehigh University with a B.A. in Journalism with a Public Relations Concentration. She will be responsible for the firm’s internal and external communications as well as promoting the business to key stakeholders.

“I’ve known Bobby personally for many years, and jumped at the opportunity to work with him,” said Lascar. "He’s a true entrepreneur and watching him grow his business from its infancy has been nothing short of inspiring. I look forward accompanying the GRWP team on its continued growth.” Early joins GRWP after a long career with Wyndham Hotels and Resorts, first serving as a Global Sales Coordinator and most recently as Executive Assistant. Amy will assist the team with client scheduling and ensuring the executive team’s time is managed efficiently.

“Green Ridge has grown exponentially. Our client base, and depth and breadth of services have been getting increasingly robust,” said Robert J. Mascia, founder and CEO of Green Ridge Wealth Planning. “Developing a team of smart, capable, and motivated people is essential to helping us realize our vision without deviating from the outstanding service we provide to our clients at every touchpoint.”

About Green Ridge Wealth Planning

Green Ridge Wealth Planning (GRWP), based in Montville, NJ, is a financial planning and investment management firm specializing in serving businesses owners, as well as individuals and clients with complex needs. As a fiduciary, the team has a legal and ethical obligation to place clients’ interests above its own. GRWP prides itself on its wealth of financial expertise, creative money management strategies, accessibility, transparency, integrity, and its culture of caring and empathy for clients and employees alike. With carefully vetted partners, including mortgage professionals, tax advisors, estate planning specialists and business strategists, GRWP can offer clients a comprehensive suite of services.

About Robert Mascia

Robert Mascia, CEO and Founder of Green Ridge Wealth Planning, is a serial entrepreneur with a unique background working both on Wall Street and as an owner of several successful businesses. Robert knew he was uniquely poised to share with business owners and entrepreneurs a wealth of financial know-how from his years of first-hand experience running businesses. That insight, combined with his love of finance, drove him to found GRWP in 2016. Today GRWP offers business owners, individuals and families a boutique, highly-personalized financial planning and investment management experience. Bobby has built a team that shares his vision and passion for excellence. The result? A growing business where clients trust the team to guide them through life’s financial complexities so that they can live their best lives.

October Commentary 2023

Why does it feel like we keep talking about the same stuff? Because the lead news and narrative remain unchanged. Why should we care? Well, because as news and variables change, we need to make sure we are digesting said news and turning it into advice for positioning portfolios. Main points to be considered:

Inflation is bad

High interest rates to borrow stinks, but to save is attractive

Stay conscious of your reentry into the markets, because timing them is a fool’s errand

Don’t get too sucked into high earnings rates as they also create idiosyncrasies in the equities market that should be capitalized on.

“If landing on the moon wasn’t dramatic enough, why should not landing on it be?” – Apollo 13

What is a soft landing? Why have economists and market experts been talking about this “hard landing” or “soft landing” ad nauseum? What the heck is going on?!?

With the Federal Reserve fighting inflation with one of the most dramatic interest-rate cycles in history, the greatest concern was the havoc that higher rates would have on the economy. In fact, more than 70% of economists were predicting a recession in either late 2022 or early 2023. And yet, no recession has been announced. Here we are, three quarters of the way through 2023, the jobs market is still strong, inflation has come down (although remains high; more on that later), and the economy seems to be trudging along. For those obsessed with aeronautics, we might call this a soft landing. We certainly would not call it a crash landing, as many were predicting (cough, cough, Michael Burry).

Even though the environment has proven to be more resilient than most forecasted, the horizon is far from clear. Oil has surged back above 90 dollars a barrel, Congress threatens another government shutdown, the consumer is showing signs of fatigue, the jobs market shows strength, but hours worked tells a more troubling story, and many economists warn that the effects of higher interest rates has yet to have its full economic impact.

That’s a lot to worry about! But it’s not all bad news. Let’s look at the bright side, when interest rates are higher, investors’ fixed-income yields are also higher. Some Money Markets are currently yielding north of 5%, an incredible return for the lowest segment of risk. That makes for a reasonable parking spot when investing discomfort sets in.

When you have a high rate of return on cash, it usually translates to a high rate of return on other assets. This is one of the positive impacts of shockingly-high inflation. It’s easy to focus on the immediate results of high inflation, but let’s not forget about the amazing returns that result after that high inflation dissipates.

In the last 120 years, we have had three periods of high inflation. The first was during World War I, and the aftermath was the Roaring Twenties. The second was during World War II, and the aftermath was the Industrial Revolution during the 1950’s. The third was between 1970 to 1983, and while the cause of the inflation ranged, the 15 years after that inflation brought annualized market returns of over 14%. High inflation doesn’t necessarily cause high returns, but it causes innovation and productivity improvements that feed the next big wave of gains in the market.

So, while cash may offer an attractive return, don’t get too comfortable sitting there for too long. There may be great returns ahead once inflation tamps down and all the amazing innovation that we are seeing matures and delivers a positive impact!

Roth IRA Versus Traditional IRA, Which is Right for You?

3 things to consider when deciding between a Roth IRA, Traditional IRA and a Roth Conversion

When planning not to run out of money in retirement, there is a lot more to consider than the current year’s tax deduction, which is the most common method for people preparing for retirement.

What are the vehicles and how do they work?

Individuals who are determining how invest for retirement are often proposed 2 options: Roth or Traditional Retirement Accounts. These 2 options usually come to the forefront of retirement planning because of the tax incentives that are associated with each. In this blog I will address the 2 types, a loophole in the IRS code, as well as the 3 things to consider when trying to determine the right option for you and your plan.

What is the difference between ROTH and Traditional?

When discussing both types of accounts, we must identify that these accounts can be either in a employee sponsored 401k or an Individual Retirement Account (IRA). The basic tax benefits are the same with a few slight differences in contribution limits as well as the 401k not having income limitations like the IRA. If making the decision in a 401k, although some of the nuances are different, the tax rules and considerations are the same.

ROTH is an account that is available to US taxpayers to help them ready for retirement. There are some basic differences that the ROTH has versus the traditional.

ROTH accounts have tax free benefits, unlike its Traditional counterpart. With the ROTH, the participant takes dollars in which they earned in the current year and contributes those dollars after tax to a retirement account. Those dollars can then be invested, most often using stocks, bonds or funds and grow tax free. Here you pay the taxes today for tax free distributions in the future.

The ROTH has income limitations when in an IRA (when in a 401k there are no income limitations). For a single person, the limit is $137,000 in gross income for the year 2020. For a married tax filer, the total household income cannot be more than $207,000 in 2020. If you make more that those amounts, you will be unable to contribute to a ROTH IRA. If you do not qualify because your income is too high, you may find benefit in a ROTH conversion, or a loophole in the IRA rules (see conversion).

Traditional IRA is also an account that is available to US taxpayers as an alternate way to prepare for retirement. Traditional IRA’s are treated differently by the IRS than its ROTH counterpart.

Traditional IRA’s are accounts in which the participant will contribute for retirement in an account that is tax-deferred. The idea is that any contributions that you make in the current year will be reduced from your income on your tax filing for the year of contribution, thereby lowering the amount of income you have to pay taxes on for that year.

Income limitations are a bit different from the ROTH. With the IRA, if you or your spouse have an employer plan available, the participant will phase out from being able to take a deduction, ultimately leading to no real benefit. Most individuals that have an employer-based plan cannot contribute to both plans, regardless if income. If there is no employer plan, there is a full deduction up to your limitations. See www.irs.gov for the different rules based upon how you file your taxes.

For both plans, they follow the same contribution limits. The maximum annual contribution for 2020 is $6000. There is a special catch-up contribution that you can make if you are over the age of 50 in the amount of $1000, totaling $7000 for individuals over 50 years of age. until the participant reaches the age 59 ½.

NOW - What are the 3 things to consider when choosing which is right for you

1. Longevity – Taxes is the biggest wealth killer in your plan. So you may have to use more than you think you will, especially if taxes are higher in the future. Given the deficit and all that is going on with COVID-19, do you feel taxes will be higher, the same, or lower in the future? Before we get into forecasting, let’s take a look at how taxes work on the money you earn, in a very basic format. We have a tiered tax system, meaning that your tax rate changes as you go up in tax brackets. If we look at 2020 tax brackets on that money, if you make $200,000, then your taxes will look something like this if you file married:

$0-$19,750 @ 10%

$19,751-$80,250 @ 12%

$80,250- $171,050 @22%

$171,050 - $200,000 @ 22%

What that means is you pay a different rate as you go up in earnings, you don’t just jump up to 22% on all $200,000. When you look at retirement, if you need to have $200,000 in order to pay your lifestyle, how do you get that money? If you are taking social security plus all tax deferred retirement accounts, all of your income is taxable, and you have to take more out on an annual basis than you thought.

But what if you had another account, like a ROTH. That leads us to…..

2. Weighting - How much you currently rely on your tax deferred dollars? In the above example, what if you could save the 22% on the $28,950 (200,000-$171,050) on an assumed distribution in 2020? Then in retirement, you have to pull out $6,369 (the 22% taxes on $28,950) less that can stay in your tax deferred account. Those are the dollars that we want to pull out in the lowest brackets, saving you on taxes. If you are contributing to a retirement account, these tax brackets play a huge role in how much to contribute to a traditional account.

A different way of looking planning which retirement account to contribute to is to consider the future possible tax rates. If we are at 22% on those dollars in 2020, what if rates go back to the year 2000’s tax brackets. If you take a 22% break today, to pay a future rate that mimics 2000, then your tax bracket would be $132,000-$200,000 @ 36% tax rate. That’s 14% additional in taxes. Perhaps taking the break today in the current environment may not be as beneficial as you thought? The good news and bad news……the current tax rates are due to sunset in 2025, meaning in 2026 we go back to the same brackets in 2015 or a new tax bracket based upon that future administration. Good news is to take advantage of the low taxes today, bad news is that those rates are not here forever. In the future, taking the deduction may be more appealing. So how can we contribute to a ROTH IRA considering above you had mentioned we cannot if we make too much money?

ROTH Conversion – The IRS has a loophole that allows you to take existing IRA dollars and convert them into a ROTH account, paying the taxes today for future tax-free distributions. Something that you should consult your financial advisor and tax advisor to see if it makes sense for your plan.

3. Inheritance – The SECURE Act was passed in December of 2019 and changed the inheritance rules around IRA’s. (Currently, and in the past, the spouse can inherit the IRA and use it as though it is theirs, so this does not apply to a spousal inheritance). In the past, a beneficiary, or the person that inherits the IRA, could take distributions based upon their life expectancy, depending on how old the decedent was at time of death. This was called a stretch-IRA, which allowed the beneficiary to draw down dollars under circumstances that could be more tax advantageous than their other 2 options; draw down in 5 years or take in one lump sum. Under the current rules, a beneficiaries longest stretch option is only up to 10 years to take the distributions to bring the account to $0. If that is a child with an already high income, those dollars get added to their current income level, possibly giving more to the IRS and less to that beneficiary. From an inheritance standpoint, tax deferred dollars are the worst to leave behind.

There is a lot to take into consideration when planning for retirement. If you have any questions on how to plan for your retirement, please reach out to schedule a free consultation with Bobby. If we are a fit for one another, we can help you to determine a map through your retirement to help you meet all of your goals and make your dream retirement a reality.

2023 Mid-Year Commentary

5 Things to know about the Market at mid-year:

The S&P is up over 13% midway through the year after being down 20% in 2022. We believe the market is forward pricing, not backward looking, so expectations are improved.

Inflation has improved, and there will be a lag of how this quick rate rise will ultimately play out. However, this is a well expected pause for the Fed on raises.

Recession fears are tough to agree with given the strong labor market and consumer strength. AI (artificial intelligence) is all the big buzz. We anticipate this as a positive for the job market, not as a damper.

There is still a ton of cash on the sidelines and the consumer has buying power.

China and Russia are concerns, but geopolitics will forever be a concern as long as there is an economic race to win. We must play the game knowing that rule.

Our industry tends to create optimists (bulls) or pessimists (bears). Both are looking for opportunity in one direction or the other. The bulls are more often right, as we have more up markets then down. However, when we have a down year, like 2022, the bears can make a lot of noise. As we always say, fear sells, so if you want to stay engaged with fear, keep watching cable news. However, it is tough to contend with the fact that this year is off to a tremendous start as we close in on halftime. The S&P 500 is up over 13% as we write this, inflation is coming down, and all of this is in the face of bank failures, debt ceilings, and recession fears.

While sometimes people confuse the market for a reflection of how the economy is doing, it is really a reflection on the expectations of investors. At the beginning of the year, investors expected the economy to be in deep recession by now, and that did not come to fruition. Everyone got a bit too pessimistic, and the rally has been the product of those investors being forced to revise their pessimism to a more optimistic view.

We may still have a recession later this year, but the rally has helped shift eyes from worrying about lower lows to thinking we might see higher highs. This is part of the reason we continue to be optimistic about the market looking forward. Many investors looked at cash yielding over 4.5% at the end of last year and felt that was the best place to be. Of course, fear and greed play a powerful role in the direction of the market, and right now a lot of professional investors are fearful that the market will hit higher levels and they will be left out as they sit in cash.

We were not as tempted as others to shift into high yielding money markets last year. We saw too much opportunity in investments that had much better long term return prospects. We felt strongly that large, cash generating technology stocks had been unfairly punished by inflation concerns, and we now see those stocks leading the market higher with a focus on cost reduction and exciting innovations in many areas such as artificial intelligence.

We also saw fixed income investments that offered returns in excess of 10%, and we have high confidence that they will pay their yields and return their principal. We remember people asking about money market rates and suggesting that as a safe haven, and our general response was “why earn 4.5% if we can earn more than twice that?” While cash always has its place in people’s portfolios and balance sheets, it is our job to find better investments than money market funds. That dedication to finding better investments with significantly higher interest rates and short durations has had a tremendous positive impact on client portfolios.

As we look forward, we actually expect much of the same:

Inflation to continue to come down

The labor market to stay strong

Companies to continue to exceed analyst estimates for earnings

The Fed to continue to not know what year or place they are in

One important difference for markets now versus the last 15 years is that the Federal Reserve’s interest rates are now relatively high. Since the financial crisis, the only stimulative measure the Fed could take was quantitative easing, or QE, since interest rates were at zero. Now that interest rates are over 5%, should the economy faulter, the Fed has plenty of room to cut interest rates, helping to slow any declines in stocks and give a boost to bonds.

So, what could go wrong? While we still think there are potential cracks in the banking system and commercial real estate, we feel most of those risks have plenty of focus and should be able to be managed without causing a crisis. The real thing that goes bump in the night for us is concern over the relationship of China and the West. This will certainly add some volatility to markets, and this should remind everyone that a disciplined process is key in an environment with so many unknowns.

But worry not, it is our job to stay up late contemplating all the risks in the world, to your investments, and your overall financial plan. If you have questions, we want to hear them. As always, we will continue to send updates both on a mass level like this note and a personal level to those we work with and help invest for.

In the meantime, enjoy your summer, and congratulations to all the graduates this year!

Bobby, Jordan, and the Green Ridge Wealth Planning Team

Green Ridge Wealth Planning is an SEC registered investment adviser. The information presented is for educational purposes only. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. Green Ridge Wealth Planning has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. FIRM NAME has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Please refer to the adviser’s ADV Part 2A for material risks disclosures. Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances of market events, nature and timing of the investments and relevant constraints of the investment. Green Ridge Wealth Planning has presented information in a fair and balanced manner. Green Ridge Wealth Planning is not giving tax, legal or accounting advice, consult a professional tax or legal representative if needed.

Executive Assistant

Green Ridge Wealth Planning

Montville, NJ

Green Ridge Wealth Planning is an independent financial planning and business consulting firm of licensed fiduciaries who work keeping our client’s best interests in mind to help guide them toward making the right financial decisions so they can reach their life goals. We advise in investments, taxes, property, retirement plans, loans, budgeting, estate planning, and wealth accumulation strategies but do not sell investment products. We also consult business owners to assist in creating a self-managed business. Clients who join the GRWP family receive white glove service.

Job Description:

We are seeking a full-time, seasoned, and detail-oriented Executive Assistant to support our CEO/Franchisee, CIO, and other members of our team. Ideally, someone who has an entrepreneurial spirit, is forward-thinking, and thrives in a fast paced, constantly evolving work environment.

Strategically manage the CEO/Franchisee and CIO’s schedules

Manage, coordinate, and follow up on complex calendars that require flexibility

Provide high quality administrative support while anticipating needs of upper management

Assist with company marketing needs

Project a professional and supportive image to clients always

Act as a liaison between owners and clients, corresponding by both phone and email

Be willing to travel locally when needed

Requirements:

College degree or 4+ years of Executive Assistant experience

Be a team player

Salary and Benefits

Competitive base salary

Paid time off after 6 months

401K with employer match after 9 months

A great mentoring program

April Commentary

April 2023 Commentary

As the second quarter of 2023 gets underway, we thought some commentary highlighting the current state of the market would be helpful. We find it useful to identify the themes we think are important and monitor those themes as the year progresses.

Before we jump into the themes, it is important to point out that the S&P 500 was up over 6% through the first quarter of 2023!

One of the major drivers of the positive return this year has been technology, while defensive and value sectors of the market have underperformed. This change in market dynamic reflects a positive shift in investor sentiment as factors that caused volatility throughout the last year have shown signs of normalizing.

There have also been new concerns that have emerged to start the year as failures among regional banks sent shocks through investors who were bracing for a wide scale banking issue. Luckily, the banking failures seem to be isolated, and the risk of a "contagion" seems low. Some of this is due to the specific nature of the banks that ran into trouble, as well as the emergency efforts to restore confidence in the banking system by regulators and government institutions.

When considering the factors that have contributed to the market’s resilience and ability to bounce back after the correction we saw in 2022, we look at themes such as inflation, the labor market, and consumer spending. All of these factors have the potential to change direction, and the financial stability in the banking system is still something to keep an eye on, but it is worth just acknowledging the current trends and expectations. Inflation One of the Federal Reserve’s core missions is to achieve price stability…or more specifically, bring inflation down to a rate of 2%. Although the inflation rate remains well above the target rate of 2%, we have seen notable improvement as we look at the progression of inflation over the last few months:

November 2022: 7.1% December 2022: 6.5% January 2023: 6.4% February 2023: 6%

As you can see in the speedometer above provided by our friends at City National Rochdale, the current outlook for inflation is neutral with a tilt towards the negative end. While we are encouraged by the direction inflation is moving, there is still ground to cover to get to the Federal Reserve's target. High interest rates and tight financial conditions will continue until the Federal Reserve feels they have a handle on inflation.

The Labor Market A low unemployment rate is one of the hallmarks of a healthy economy. As we look at the recent labor market data, we are encouraged by the resilience we are seeing.

December 2022: 3.5% unemployment January 2023: 3.4% unemployment February 2023: 3.6% unemployment March 2023: 3.5% unemployment

For some context on the above numbers, the average unemployment going back to 1948 has been 5.73%. The current rate of 3.5% is near an all-time low. The current outlook for the labor market as outlined above is neutral with a lean towards positive. While unemployment remains at a historically low level, the number of jobs being added to the economy per month is decreasing, as is the growth in employee wages. Overall, we believe the labor market is strong which increases the possibility of the fed pulling off a "soft landing" which refers to their ability to tighten financial conditions without inducing a significant recession.

Consumer Spending Consumers are the largest driver of the U.S economy and their spending habits have a large impact on overall economic activity. Consumption accounts for around 68% of the GDP (Gross Domestic Product) calculation. While most think of a rapidly growing GDP as a sign of a healthy and booming economy, it can also contribute to the inflation issue. If consumers are spending at record levels, demand for goods will be higher, which in turn can make it harder for inflation to moderate.

As we look at the PCE index (personal consumption expenditures) we can see that consumer spending is continuing to grow over time, but at a slower rate than it was previously. This may be the sweet spot that allows inflation to moderate while stimulating the economy enough to avoid a significant recession

The current outlook for consumer spending as outlined above is neutral. While it is ideal for consumer spending to be increasing at a slower rate, there is risk for it to start trending in a negative direction month over month if financial conditions continue to tighten. An example of financial conditions tightening further would be if the Federal Reserve continued to raise rates throughout 2023.

The economic themes outlined above all seem to be progressing well, as can be seen in the reaction of the market. However, in the near term, we do expect more volatility as new data comes in and the Federal Reserve weighs its options. There are still many opportunities to be found in the market between high yield structured notes, equities that have fallen way off their all-time highs, and low risk securities like CDs and money market funds providing attractive yields.

We hope this commentary provided some context on the state of the market! Please feel free to reach out to our team if you have any questions.

Cash Management: How to Make the Most of your Savings in the Current Environment

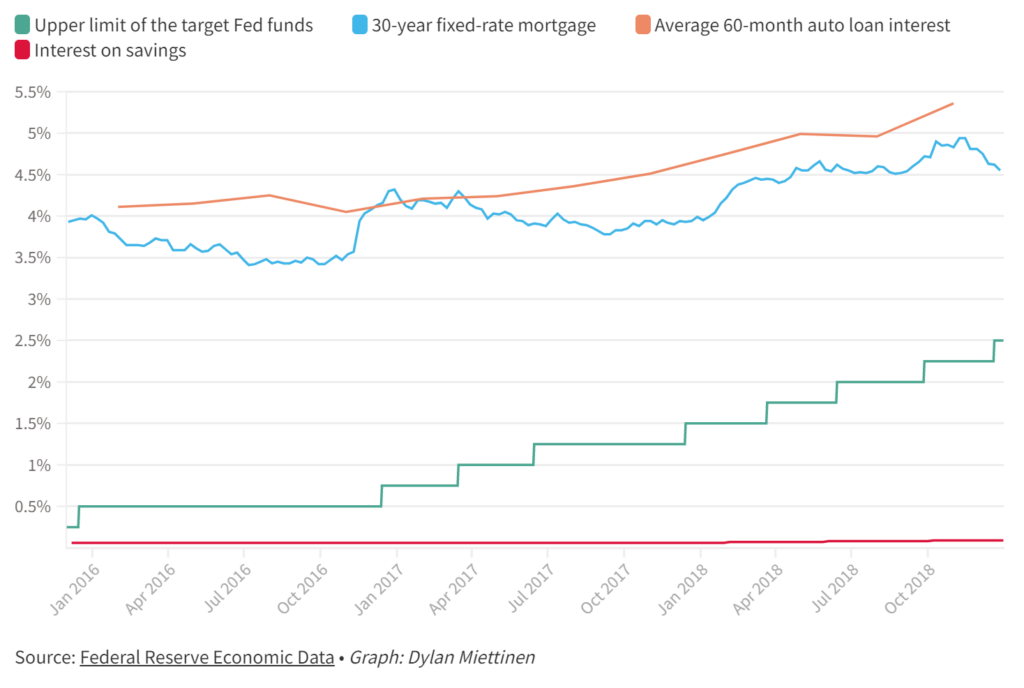

It is no secret that the stock market has experienced a great deal of volatility since the start of 2022. The declines we have seen in the markets recently have created an appealing opportunity set among both equity and fixed income securities. With prominent indexes like the S&P 500, NASDAQ, and Barclays Aggregate Bond Index all trading at significant discounts compared to where they were in late 2021, we think it is a great time to be invested to capitalize on potential upside. However, the current environment has also made investors rethink how they are treating excess savings with the reemergence of attractive rates among Money Market Funds, Certificates of Deposit, and Treasury Bills.

One of the largest headwinds we have been facing in the economy over the last 18 months is an abnormally high and stubborn inflation number that has eaten away at consumers purchasing power. This has forced the Federal Reserve to react by increasing interest rates, thereby slowing the economy and inflation. A positive byproduct of these rate raises is a market that is now rewarding investors for lending out their money. By utilizing vehicles such as Money Market Funds, CDs, and Treasury Bills, investors can earn annual interest in excess of 4% without experiencing the volatility of the equity market.

The chart above demonstrates how the federal funds rate has changed over the last 1 year. After the most recent .25% rate hike this month, the federal funds rate sits just below 5%. The cash management vehicles discussed above such as Money Market Funds, CDs, and Treasury Bills tend to have yields in the same ballpark as the federal funds rate.

While moving funds out of equities or high yielding fixed income instruments into these traditionally safer vehicles is not generally advisable after a downturn, it has become an attractive opportunity for investors with cash stockpiled in low interest bank accounts that are looking to avoid the volatility of the market. This approach to cash management when utilized on savings in excess of 3-6 months of living expenses can be a great way to earn some interest on funds that are sitting on the sideline.

Structured Notes

For those willing to take on a bit more risk in their cash management strategy, structured note products can be utilized or combined with the vehicles outlined above to achieve a higher overall yield. Creating a combination of notes and treasury like securities can be another great way to earn competitive returns on cash that would otherwise be earning very little in a bank account. Equities remain the space with the highest overall return potential, especially after the downturn we have experienced, but there are now other ways to take advantage of the current environment.

Feel free to reach out to our team if you have any questions about cash management or investments in general.

Now Hiring: Staff Accountant

Job Role: We are looking for a detail-oriented Staff Accountant to complete general accounting and financial tasks, including assisting in the development of processes, for the organization. In addition to the daily accounting and financial entries to be made, you will also carry out relevant administrative duties, such as interacting with store managers and communicating with other essential parties.

The ideal candidate will be a highly organized, problem solver able to work independently and efficiently to ensure the company’s financial record keeping is accurate and complete; must be energetic, personable, and fun to work with; must possess an entrepreneurial spirit and embrace a fast paced, constantly evolving environment. This position reports directly to the organization’s Controller.

Responsibilities:

Enter daily sales transactions in QuickBooks Online for multiple entities.

Obtain and accrue inventory sheets from store managers on a monthly basis.

Keep track of payroll reimbursements between several entities.

Perform monthly bank reconciliations for multiple accounts.

Run weekly sales reports and report information to Dunkin’ Brands for the payment of franchise fees; record same in the entities’ general ledgers appropriately.

Pay weekly invoices for multiple entities.

Enter weekly ACH payments for product and delivery from bakery to Dunkin’ locations outside of the MCG Dunkin’ group.

Assist with documentation and file creation for all audits.

Maintain and update accounting records and files, as necessary.

Conduct month-end and year-end accounting closures.

Adhere to internal and industry accounting policies and standards and ensure compliance with rules and regulations.

Create reports for upper management as needed.

Requirements and Skills:

Excellent verbal and written communication skills.

Excellent organizational skills and attention to detail.

Knowledge of general financial accounting and cost accounting.

Understanding of and the ability to adhere to generally accepted accounting principles.

Highly Proficient with Microsoft Office Suite, QuickBooks Online and accounting software.

Education and Experience:

Bachelors degree in Accounting, or related field, required.

At least three years of related experience required.

Physical Requirements:

Prolonged periods sitting at a desk and working on a computer.

Must be able to lift up to 15 pounds at times.

NOW HIRING: Financial Advisor

Green Ridge Wealth Planning, LLC, a financial planning and investment management firm delivering Wall Street experience, with a Main Street mindset, is seeking an experienced Financial Advisor to join our dynamic team. This is your chance to play a key role in the current and future success of this fast-growing organization!

We need a team member excited to take on financial planning, wealth management, client relations management and development – someone who is seeking an opportunity to strategically support existing and new clients in preserving and growing their wealth.

Duties & Responsibilities

Provide premier service to clients by preparing for meetings, providing thorough investment and manager research, problem solving, resolving issues, and making financial planning recommendations.

Develop effective working relationships with internal team members and external professionals to provide effective service.

Conduct and memorialize communications with clients and/or prospective clients.

Manage, organize, and present data accurately and succinctly and review that data on a weekly/monthly/quarterly basis.

Attend client and team meetings, document discussions, assign tasks and execute on follow-up.

Assist in nurturing the firm’s relationships with new clients.

Qualifications

Our team members succeed by performing all duties and responsibilities with enthusiasm and the utmost integrity. The requirements listed below are representative of the knowledge, skill, and/or ability required to succeed on our team. Reasonable accommodations may be made to enable individuals with disabilities to perform the essential functions.

Strong interpersonal and communication skills to deal with financial advisors, support staff, and vendor companies in all types of matters, including those that may be sensitive.

Comprehensive understanding of company policies and procedures and industry rules and regulations.

Ability to project a professional and pleasant demeanor to advisors, teammembers, and clients in a deadline-driven environment.

Commitment to providing a premier level of customer care in a calm and professional manner.

Ability to effectively organize, manage, track and complete multiple detailed tasks and assignments simultaneously.

Employ solid analytical skills in researching and resolving problems.

Work independently with minimal supervision.

Produce and maintain extensive documentation of all client and internal communications.

Operate effectively and with the highest integrity for our office and clients; never taking shortcuts and adhering to all Compliance rules.

Utilize financial platforms including Wealthport, eMoney, Redtail, Riskalyze, and Microsoft Office Suite.

Demonstrate the ability to build trust-based relationships with clients.

Education/Previous Experience Requirements

Bachelor’s degree and a minimum of four (4) years of experience in the financial services industry -or- an equivalent combination of experience, education, and/or training as approved by the firm.

Licenses/Certifications

FINRA Series 7, Series 65 required with a commitment to obtaining further continuing education requirements to maintain licensing.

Job Type:

Full-time Salary plus bonus based on experience

Benefits:

401(k)

Health insurance

Paid time off

Physical setting:

Montville Office

Schedule:

Monday to Friday

Market Commentary 2/23

Wow, what a start to 2023!! After an extremely challenging year, we are seeing a very different type of market as we shed some of the concerns that drove the market lower in 2022. Inflation is cooling, the Fed is nearing the end of its rate hike cycle, China is coming to its senses, and Europe seems to be managing through the winter with the conflict in Ukraine.

Investors who held in there are starting to see some recovery after the carnage of the last 12 months. The last year though has really been a tale of two halves;

The first six months of 2022 were nothing but a straight slide down. Everyday we saw more red and continued declines.

The last 6 months of 2022 were choppy, but generally flat. The real turning point was a slight tick down in inflation, and from there, the market tried to see past the economic weakness, Fed policy, and other difficult headlines that seemed to roll in every week.

With the big rally we saw in January, the last 6 months are starting to look downright good. I know that sounds crazy, but the numbers don’t lie. And with market strategists at major financial institutions still predicting a difficult year for markets, it begs to wonder if the recent strength can hold together or if we are just setting ourselves up for another slide down.

And there lies the main question on every investors mind; are we going to see a bounce back in the market in the near term, or are we going to have a prolonged downturn that continues to turn account values and stomachs.

We at Green Ridge are bullish! “Why?”, you might ask. While we don’t have a crystal ball, we do have eyes and ears. What we see is more and more indices, sectors, and individual stocks starting to develop bullish patterns and upward momentum. Take a look at the general technology sector. Beat down over 27% last year and up almost 10% on the year. What we hear is continued skepticism from wall street professionals. That contrarianism is just the same as when markets are boiling over. It goes too far before all the institutions that are currently skeptics become frantic buyers if they have a change of heart and move to the bull camp. Both of these things can change on a dime, but history has taught us to trust our eyes more than our ears.

So, what do you do? We think it always makes sense to remain level headed and stick to your long term strategy. There are opportunities in the market right now all over the place, and while all of those opportunities might not make sense for you given your risk tolerance and time horizon, we see a solution for all types of investors. If you are having trouble seeing them, or feel like you want to learn more about what we are seeing and why we feel so optimistic, give us a call! We love gabbing about this stuff!!!

Hang in there, and know that there are brighter days ahead. Maybe not tomorrow, but then the day after that!

September Commentary: What are you afraid of?

GRWP Hot Points of Discussion:

We have been heavily defensive long enough. It’s time to start looking optimistic and bullish, both in the near-term (next 6 months) and the long-term (over 3 years).

The first half of this year was very challenging for markets, and while it had its own unique characteristics, it was not totally unexpected or especially unusual.

As we look forward, our fear is missing an opportunity. That doesn’t mean we throw risk concerns out the window, but instead just means we pivot from defense to offense.

It has been nothing short of a crazy year so far! Whether you watch markets or headlines, it is near impossible to keep your sanity these days. And add a midterm election cycle and inflation concerns and it really feels like nothing can go right....... And that makes me so positive on what is going to happen next! Seem crazy? Maybe not, give me a chance to tell you why.

To give some context here, I want to share a bit of a rule system that I think makes for a great investor. Bobby would hit me over the head if I got technical on this, so these rules are left in the laymen.

The K.I.S.S. method......Don’t overthink it! Markets are down, and history has taught us take advantage of lower prices.

So much bad news is baked into the cake. Sentiment is a major factor in what happens with prices.

When sentiment gets too positive, things tend to get more difficult. Good news is expected, and bad news comes as a major shock.

When sentiment gets too negative (as it is now), bad news is shrugged off. Good news becomes unexpected, and causes big swings to the upside.

While we all want to make predictions about the future, we have no idea what will happen (no one does!). So with that regard, please refer to rules 1 and 2.

So here we are, in an environment that is decidedly negative, with prices that are lower, and an environment that is as unpredictable as I can ever remember it being. But think about other times where the outlook was bleak: