Four Retirement Plan Options for Business Owners

Being a successful business owner is an extraordinary accomplishment. As our CEO, Bobby Mascia, likes to say, business owners wear many different hats. At Green Ridge, we like to unburden some of those responsibilities from clients so that they can focus on the most important aspects of their businesses and lives.

One way is by working with your other professionals, like your CPA, to ensure your retirement plans are best suited to your circumstances and needs. The information below breaks down retirement plans outside your 401(k) and the pros and cons of each.

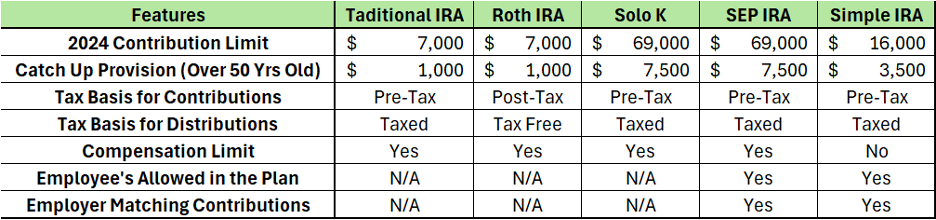

Traditional IRA

Pros: Easy to set up and very flexible. You can rollover funds from previous retirement accounts.

Con: Low contribution limits.

ROTH IRA

Pros: Similar to a Traditional IRA, it is easy to set up and very flexible. You can also rollover funds from a previous ROTH retirement account. Your contributions are made post-tax so when you take your distributions at retirement, they are tax-free.

Cons: Low contribution limits and ROTH IRAs have compensation limits.

- If filing as a single person your MAGI (Modified Adjusted Gross Income) must be under $146,000 for tax year 2024 and if filing as married your MAGI must be less than $230,000 for tax year 2024 to be able to contribute to a ROTH IRA.

Solo K

Pro: High contribution limit.

Cons: You can only use this type of retirement plan if you have no employees. However, your spouse can also contribute to this plan. You must file paperwork with the IRS once the account value is $250,000 or more.

- Since you are the employer and the employee, there are two parts to the contribution strategy:

- As an employer you can make an additional contribution of up to 25% of your compensation.

- As the employee you can contribute up to $23,000 in 2024; similar to regular 401(k) plans.

- Special rule for sole proprietors and single-member LLC’s: You can contribute 25% of net self-employment income.

SEP IRA (Simplified Employee Pension)

Pro: High contribution limit.

Cons: As your business grows and adds employees, you must contribute the same percentage to all eligible employees as you do for yourself.

Example: If you contribute 15% to your SEP IRA you must also contribute 15% to all eligible employees' SEP IRA, which could become costly as your business grows.

Simple IRA

Pros: Higher contribution limit than a Traditional or ROTH IRA. Low account administrative involvement and an easy plan to start, similar to a Traditional IRA.

Con: Employers are generally required to either make matching contributions of up to 3% or fixed contributions of 2% to every eligible employee.

There are other options available to business owners than a 401(k), which is often the first option that comes to mind and may not be the best fit given your specific circumstances. As you grow, there are multiple options available to you and is important to walk through each one to determine which will provide you with the most value. As we mentioned above, another crucial factor is having all your professionals collaborating as a team to coordinate strategy among the types of accounts, tax strategies, and funding options.

Green Ridge Wealth Planning, LLC is a registered investment adviser. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment / tax advice. The investment / tax strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment / tax strategy for his or her own particular situation before making any investment decision. You are responsible for consulting your own investment and/or tax advisor as to the consequences associated with any investment.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of AUTHOR, may differ from the views or opinions expressed by other areas of Green Ridge Wealth Planning, LLC, and are only for general informational purposes as of the date indicated.